Quantitative Tightening has removed 38% of Treasury securities and 27% of MBS that pandemic QE had added.

By Wolf Richter for WOLF STREET.

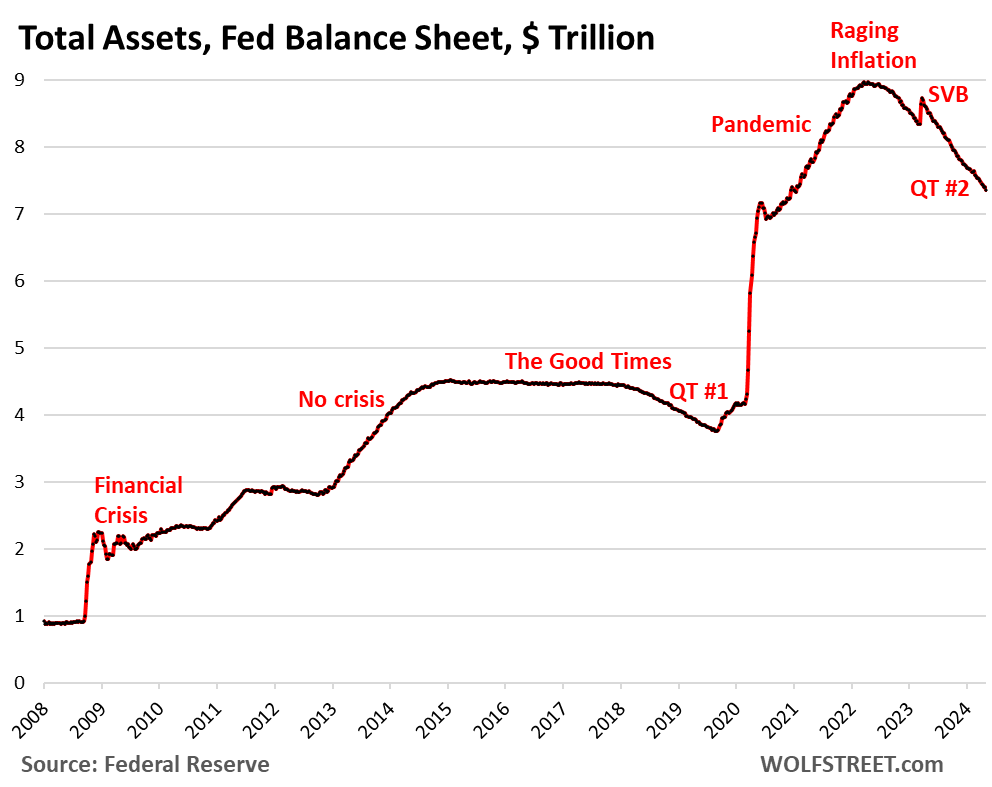

Total assets on the Fed’s balance sheet fell by $77 billion in April, to $7.36 trillion, the lowest since December 2020, according to the Fed’s weekly balance sheet today. Since the end of QE in April 2022, the Fed has shed $1.60 trillion.

After months of talking about it, the Fed has now clarified officially when, how, and by how much it will slow QT. They’re trying to get the balance sheet down as far as possible without blowing anything up, and easy will do it, that’s the hope.

- Starts in June

- Cap for Treasury runoff reduced to $25 billion from $60 billion

- Cap for MBS runoff unchanged at $35 billion

- If MBS run off faster than $35 billion a month, then the excess will be replaced with Treasury securities, and not MBS.

- MBS to essentially vanish from the balance sheet over the “longer term.”

QT by category.

Treasury securities: -$57 billion in April, -$1.25 trillion from peak in June 2022, to $4.52 trillion, the lowest since October 2020.

The Fed has now shed 38% of the $3.27 trillion in Treasury securities that it had added during pandemic QE.

Treasury notes (2- to 10-year securities) and Treasury bonds (20- & 30-year securities) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. The roll-off is capped at $60 billion per month, and about that much has been rolling off, minus the inflation protection the Fed earns on Treasury Inflation Protected Securities (TIPS) which is added to the principal of the TIPS.

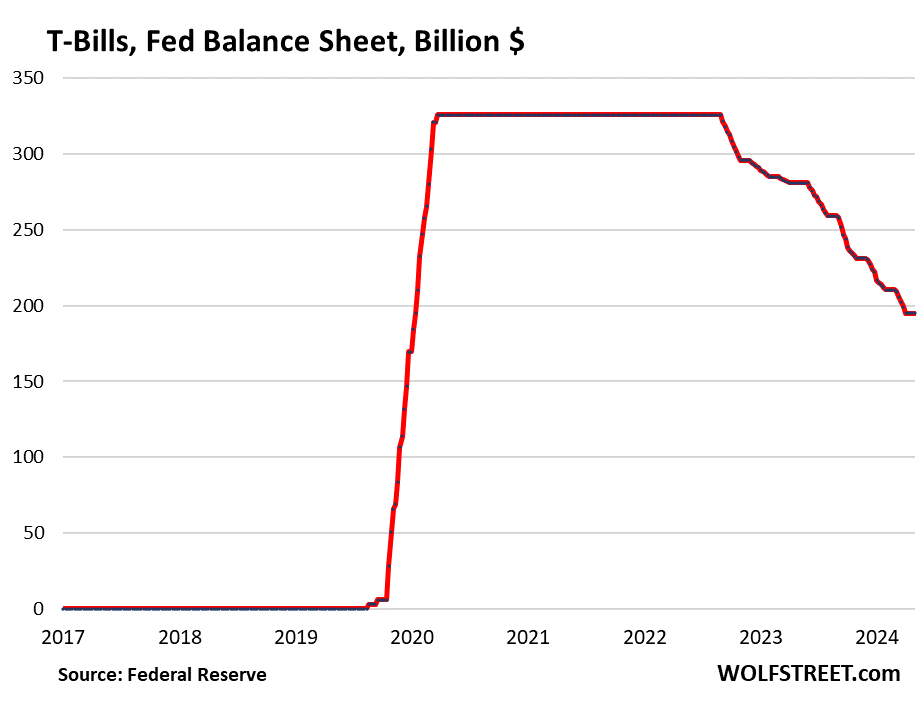

Treasury bills. Unchanged in April at $195 billion. These securities with terms of up to 1 year are included in the $4.52 trillion of Treasury securities on the Fed’s balance sheet. But they play a special role in QT.

The Fed lets them roll off (doesn’t replace them when they mature) only if not enough longer-term Treasury securities mature to get to the $60-billion monthly cap. This allowed the Fed shed about $60 billion in Treasury securities every month.

From March 2020 through the ramp-up of QT, the Fed held $326 billion in T-bills that it constantly replaced as they matured (flat line in the chart below).

The slower QT starting in June will follow the same principle with T-bills. But the first month with a Treasury roll-off below the new cap of $25 billion is September 2025 ($17 billion). So T-bills will stay on the balance sheet unchanged at $195 billion until then, even as notes and bonds come off:

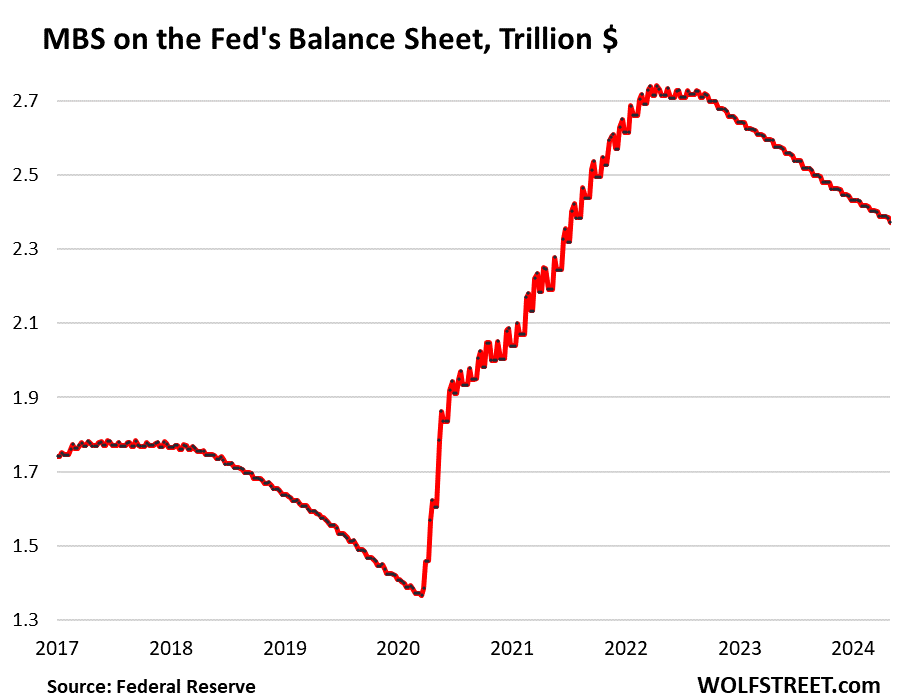

Mortgage-Backed Securities (MBS): -$16 billion in April, -$368 billion from the peak, to $2.37 trillion, the lowest since July 2021. The Fed has shed 27% of the MBS it had added during pandemic QE.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made.

But sales of existing homes have plunged, and mortgage refinancing has collapsed, and so fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have been reduced to a trickle, and the MBS are coming off the balance sheet at a pace that’s far below the $35-billion cap.

Under the slower QT starting in June, the MBS cap remains at $35 billion. When the housing market unfreezes, and sales volume rises to more normal-ish levels, mortgage payoffs will increase, and therefore passthrough principal payments to MBS holders will increase, and the MBS roll-off will increase from current levels, and the curve in the chart below will steepen.

If pass-through principal payments exceed $35 billion – during the pandemic housing boom, they exceeded $110 billion in many months – the overage will be replaced with Treasury securities, not MBS, as the Fed wants to phase out the MBS on its balance sheet.

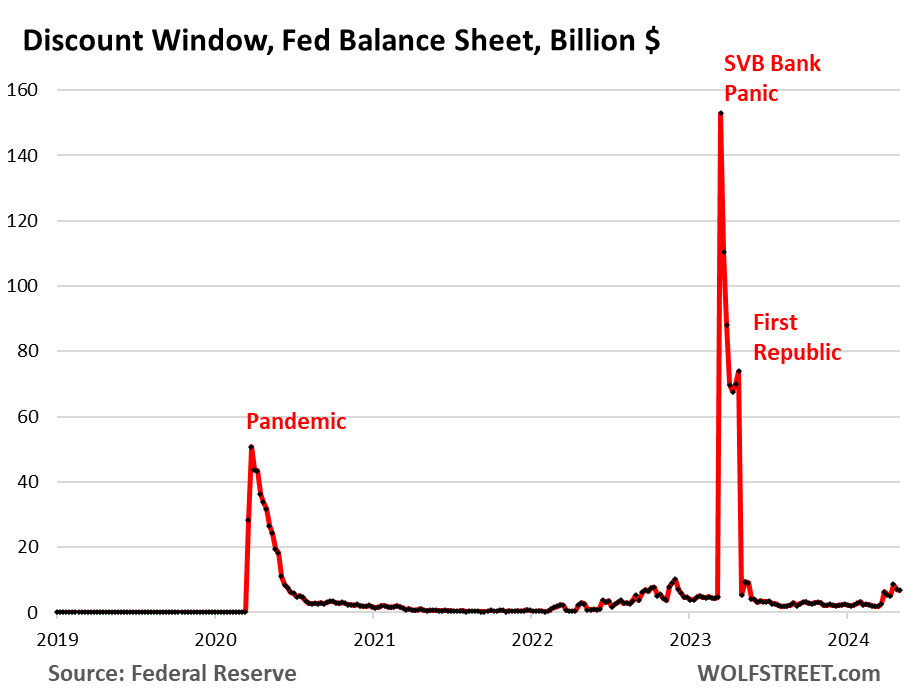

Bank liquidity facilities.

Discount Window: +$1.3 billion in April, to $6.8 billion. During the bank panic in March 2023, loans had briefly spiked to $153 billion.

The Discount Window is the Fed’s classic liquidity supply to banks. The Fed currently charges banks 5.5% in interest on these loans – one of its five policy rates – and demands collateral at market value, which is expensive money for banks, and there’s a stigma attached to borrowing at the Discount Window, and so banks don’t use this facility unless they need to, though the Fed has been exhorting them to make more regular use of this facility.

Bank Term Funding Program (BTFP): -$6.4 billion in April, to $124 billion.

Cobbled together over a panicky weekend in March 2023 after SVB had failed, the BTFP had a fatal flaw: Its rate was based on a market rate. When Rate-Cut Mania kicked off in November 2023, market rates plunged even as the Fed held its policy rates steady, including the 5.4% it pays banks on reserves. Some smaller banks then used the BTFP for arbitrage profits, borrowing at the BTFP at a lower market rate and then leaving the cash in their reserve account at the Fed to earn 5.4%. This arbitrage caused the BTFP balances to spike to $168 billion.

Frustrated by seeing the BTFP abused for profits, the Fed shut down the arbitrage opportunity in January by changing the rate. It also let the BTFP expire on March 11. Loans that were taken out before March 11 can still be carried for a year. By March 11, 2025, the BTFP will be zero.

The balance sheet after 12 months of slower QT.

In May, the Fed will shed another $75 billion or so in assets, which will bring the balance sheet down to roughly $7.28 trillion. In June, the slower QT sets in. After the first 12 months of slower QT, so by the end of May 2025, total assets might be lower by these amounts:

- If MBS passthrough principal payments continue at $15 billion a month, instead of speeding up, it would remove $180 billion by the end of May 2025.

- The $25 billion in Treasury roll-off would remove $300 billion by the end of May 2025.

- The BTFP will go to zero by March 2025, which will mop up $124 billion.

- Unamortized premiums are taking off $2.2 billion a month, or $26 billion in 12 months.

- Total: minus $630 billion by end of May 2025.

So without acceleration of the MBS roll-off, the balance sheet would be down to about $6.63 trillion by the end of May 2025.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

A balance sheet of $7.36 Trillion remaining is a sickening and disgusting indictment on unelected, incompetent and arrogant bureaucrats who have sold out the ordinary American people.

“A balance sheet of $7.36 Trillion remaining ”

It’s down by $1.6 trillion. What’s your effing problem? That’s far more than anyone including me was dreaming about 2 years ago.

It’ll be down by $2.2 trillion, dropping to $6.6 trillion, by the end of May 2025, with the slower QT and all, as explained in the article.

Wolf,

Don’t ban me. I admire your work.

But I agree with Marco.

True Fed is cleaning up their 4 decades of reckless policies. But it’s their mess to clean up. May be they’re just preparing for the next crony capitalism event. Who knows. I lack confidence personally. And the Fed’s debt mess is a tiny fraction of the debt overhang created.

Not the only constuient in the construction of this massive collective fuduciary fail: goverance, fiscal, monetary, social, economic, judiciary, regulatory, media.

Some good people out there, too. But what a mess has been created by others.

Sure. blame the Fed for QE. No problem. But this isn’t QE. This is QT, if you haven’t noticed. Don’t blame them for QT. I’m tired of this BS that $1.6 trillion in QT and ongoing is like nothing. Spread QT denier BS on ZH. It will get deleted here. I’m not wasting my time on it anymore. I’m sick of it after two years of copy-and-paste QT-denier BS on every article about QT.

I agree. The Fed has enabled extremely bad behavior on a scale humanity has never seen before. If we truly had a representative republic their charter would be revoked and the management of all member banks since 2001 criminally prosecuted.

The majority of the debt they created was not approved by “we the people” as our representation has been fully captured by the same banks and their MIC whores. Follow the money, this isn’t rocket science. Now good money will chase out the bad. Instead of prosecuting FRAUD (i.e. MBS) and allowing bad debt to clear and bad management to go bankrupt The Fed and CONgress rewarded these same entities with bailouts. Now we get a hyperinflationary depression and more likely war in order to hide all this nefarious behavior.

NYTimes columnist Jeff Sommer today also suggests the QT pace is too slow

Since Fed bond holdings are still above the COVID-induced bump but the economically disruptive effects of the pandemic are over, you’d think that unless there are new systemic weaknesses known to the Fed, that they would continue with QT at the rate it was going, rather than slowing by 50%.

So maybe there are new systemic weaknesses known to the Fed and they are not saying

Wolf,

It’s OK if you ban me. I don’t really belong in this peanut gallery anyway.

I share Marco’s sentiment. I would add, I have lost faith in the Fed when they did QE, bought MBS, & treasuries. Literally, I would not be surprised next QE if the buy equities.

Love your web site! Huge fan!

Keep up the great work

@Sacramento,

Japan was buying equities with their QE a few years back

my effing problem is that the Fed exists

It’s an institution of the United States, set up by Congress. There are lots of things some people don’t like. But it’s the system we have. If you don’t like the Fed as an institution, go move to Japan, they’re still at 0% and doing QE, LOL

Do you rage at motorized automobiles and modern vaccines? Do you want to go back to horse drawn carriages and leeches?

I ask because the FED is every bit a technological advancement as medicine and the auto.

There is a reason why literally every 1st world economy has a central bank. You may not appreciate why this is, but your rage isn’t going to get rid of the FED anymore than it is going to get rid of the auto.

We’ve had an economy without the Fed before. The results weren’t very good either.

The thing about central banks is that they cannot fix bad government. If governments don’t regulate financial markets, don’t have good long term planning, don’t invest wisely, and do things like implement austerity policies during downturns and refuse to raise taxes to balance budgets, then the central bank ends up having to do stupid things to maintain dollar stability. I do think the central banks in many countries have been very poorly run, but they also have very few options.

Part of the reason central banks were made independent was so the govt could blame the central bank for dishing out the necessary bad medicine rather than doing it themselves and then losing the next election. But if you have govt that doesn’t really want to take the medicine then this mechanism eventually breaks down as well. IMHO that is what we are seeing in the west.

Just because the US Government does something, like create a Fed, doesn’t mean it is legal.

Thomas Jefferson and Andrew Jackson ended the “Feds” of their day. Like it’s predecessors, this Fed can and certainly will be ended.

I rage against the Fed, fiat currency, bailouts and violations of the Constitution of the United States and violations of natural rights.

The existence of the Fed, fiat currency & bailouts, is anti-American. These things create inequality. These things are unnecessary and have greatly harmed my family and hundreds of millions of other people.

There is nothing novel, technological or modern about the Fed. It is an old pre-industrial racket perfected in the age of feudalism.

This is such an insane take. Are we going to go back to the gold standard too?

Many years ago, I would go see the circus when it came to town. It was quite the spectacle.

At some point in the circus, there would be a parade of the animals. It took place in the center ring and it was a big deal. There were two guys, one on each side. Their job was to keep the animals moving in an orderly manner. They also had a shovel, a broom and a mop. Inevitably one or more of the animals would relieve themselves. sometimes spectacularly.

Those guys were the Fed of the circus. they were not the circus. the circus is the legislators, the administration, the wall street criminals. You anti Fed guys got it all wrong. Thank god for the fed.

LOL crazies determining what is legal.

Again, modern banking is no different than modern automobiles. No sane person wants to go back to pre-central bank banking, just like no sane person wants to go back to horse drawn carriages as the primary means of transportation.

Just answer the simple question.

Given that every single 1st world country has a central bank, heck even a vast majority of 2nd and 3rd world counties have central banks, why is it wrong for the U.S. to do do?

I am pretty sure people are just blindly looking at the FED’S balance sheet and comparing it to the balance sheet prior to QE without realizing that there are some rather large differences in the balance sheet now versus pre-QE that have absolutely nothing to do with QE.

An increase in the physical money supply and the government moving their checking account to the FED (from Chase) are the two biggest.

They simply do not realize that the FED’s balance sheet would have grown much larger even without QE.

Also, banks don’t lend to each other anymore. They borrow from, and lend to the Fed.

Another example of irony: the FFR is the “key policy rate” yet the interbank market is basically dead.

Wolf does a good job highlighting those issues when he does liability articles.

Central banks may not be bad in all cases but they ARE if they’ve done what this Fed has done in coordination with Congress, the Administration, and the Treasury which is perpetually enabling the gov’t to spend more than its revenues and create more money than the increase in production of goods and services which debases the value of the dollar. So, because they follow the orders of their debt monger political donors, voting for the Republicans or the Democrats is voting YES for MORE inflation. But just like all the previous nations and empires that tried and failed, we can’t create net production and prosperity with money printing and debt. And saving something smaller from “blowing up” now by giving the junkie another hit will only lead to something bigger blowing up in the future. But most people don’t realize the mess their children and grandchildren will be in because “debts don’t matter until they do”.

While I agree with you on everything else, wouldn’t you agree that the current Fed went overboard with their purchase of MBS? Isn’t this outside their mandate? Isn’t this largely responsible for the housing bubble?

tyaresun,

Absolutely. It should have NEVER bought any MBS ever. It should have never done QE with bond purchases. It should have used repos to deal with market problems (GFC and pandemic), as it used to do before 2008. That would have worked fine. Those repos would be gone after a couple of months, as markets go back to normal. That’s what it did during 9/11, as markets were actually shut down for a few days, and chaos ensued, and it doused the markets with liquidity via repos for a few days, and after a couple of months, the repos were gone, and the dotcom bust continued.

Financial Crisis QE is ancient history. 2008 was 15 years ago. Pandemic QE was years ago. Whatever it did, it did. Water under the bridge. Now we have QT, the biggest ever, $1.6 trillion so far, and people are blaming the Fed for QT. The Fed is finally and for once doing the right thing. The enemy is 0% and QE, not 5.5% and QT.

Wolf,

I do not disagree with you that the FED should not have done MBS purchases, or QE at all. Absolutely no doubt or argument. I hate that it happened.

However…..

During the housing crisis, the MBS market absolutely locked up. It was partially a liquidity issue, but more than that it was an informational issue. None of the market participants knew what the MBSs already on their balance sheet were worth because there was no market to give them prices. Since they didn’t even know their own balance sheets, there was no way they could enter the market to buy more.

Most of this wasn’t even MBSs, it was derivatives based off of MBSs. Literally no one knew who was solvent and who wasn’t. An insured MBSs was worthless if the insurance backing it was iffy.

Basically there was a huge need for entities that were not normally MBS buyers to enter the market.

There were all sorts of plans floated to enable this. Even at the highest levels. One was to enable very well capitalized entities (think Buffett) to be able to put up their own capital and also borrow at rock bottom rates (better than the Federal government) and have those loans backed by the federal government, while they would share the eventual winnings with the government. They would then buy MBS and restart the market.

This was the plan until someone realized that this could easily be framed as a giveaway to the rich. So it was scrapped.

Other plans were put forward but all of them required well capitalized buyers who didn’t normally participate in the MBS market. All of them had political issues. There was also the problem that all of them were going to take time to set up. Other than Buffett, the FED, or the federal government, there is no one who can wire $25 billion into an account instantly. Time and political pressures were immense. No solution was going to be easy.

So the solution was to have the FED buy MBSs and loosen the market. They were well capitalized (technically infinitely capitalized), it could be done instantly, and the political problems would come far later.

It was a horrible solution, but it MIGHT have been the only possible solution.

Maybe not, but maybe so.

Waiting for the MBS (and insured market) to sort themselves out probably would have meant millions of unnecessary job losses, a recession that was far worse than actually happened, and potentially a 2nd great depression.

As much as I don’t like the FED buying MBSs, I cannot say I wouldn’t have done anything different at the time if I was in charge. It was a bad time with no good choices.

That said, the FED really screwed up by not unwinding this ASAP. There was no reason that they couldn’t have been actively selling MBSs into the market in 2012 (or later). Would have it influenced the MBS market? Of course. But no more than their pirchases did. The fact that they continued these emergency measures for over a decade is a joke.

JimL,

Your MBS theory is wrong because there were two different things, and it seems you mixed them together:

1. The MBS that the Fed bought as an emergency measure were private-label (not government guaranteed) MBS that were selling for 10 to 40 cents on the dollar. The Fed bought a few tens of billions of dollars of them and stuck them in LLCs on its balance sheet, called “Maiden Lane I,” “Maiden Lane II,” etc. to let them rot off the balance sheet over the years, or sell them if they didn’t rot off. Look up: Fed balance sheet Maiden Lane. That wasn’t part of QE. By 2018, the Fed had SOLD the last one of them. SOLD outright. And made money. That was not QE; that was designed to get markets to function again.

2. Under QE, the Fed bought only government guaranteed MBS with no credit risk and put those on the balance sheet the proper way, but it bought $1.8 TRILLION of them by 2014, and they’re not rotting off, and the Fed isn’t selling them. The purpose was to inflate asset prices, particularly home prices. That was QE.

@ Wolf –

Thanks for straightening out the JimL story and those of us who might have been mis-led by it.

An aside: Though the FED may have made money off of the Maiden Lanes, would that have been possible withou the $1.8 trillion purchase of Government guaranteed MBS, that the FED did to manipulate housing prices higher?

Also, when the FED bought the Maiden Lanes, though it might not have been part of the FED’s formal QE, did they not purchase Maiden Lanes with newly created money that did at least temporarily expand the money supply?

cb,

Your last paragraph: sure, but that wasn’t QE. It had a very different purpose, and those things were gone after the crisis was over – similar to repos (which can come off even faster, in days or weeks). QE is designed to inflate asset prices, not fix market dislocations. But the short-term liquidity effects can be similar.

Wolf said: “QE is designed to inflate asset prices, not fix market dislocations.”

————————————–

Thanks for this clarification. It helps me, and I suspect others, better understand your overall picture.

When some of us see new money creation I think it easy to assume that QE continues as convenient. You point out a reason not to hastily ump to that conclusion.

Wouldn’t all these reactions fall into a classic Overton shift? If the Fed ran its balance sheet to $8.8 T and then pounds its chest by reducing it by 25% or more, they think we are all happy campers. But over twenty years, it has been up by unfathomable amounts that we have now forgotten about. So we have a new window of comfort.

Do you have a 50-year Fed balance sheet chart to see just how far they have pushed the window of comfort over time?

Jamie60,

This is all nonsense. In 1976, the balance sheet was about $100 billion. And it grew steadily to $900 billion by 2008, before QE started, so that’s an 800% increase. It increased dollar for dollar with currency in circulation (paper dollars), which are a liability for the Fed, and must be balanced by assets for the balance sheet to balance. During that time, relatively speaking, the balance sheet remained at about 6% of GDP.

Since 2008, the balance sheet must grow not only with currency in circulation but also with the TGA. This is the government’s checking account that was moved from JPM and other banks to the New York Fed during the financial crisis and has therefore been on the balance sheet since then. Both currency in circulation and the TGA are a liability for the Fed, and assets MUST balance liabilities dollar for dollar when capital is fixed — which the Fed’s capital is — so that the balance sheet balances.

The problem we had were the two phases of QE (2008-2014 and 2020-2022).

READ THIS — people MUST read these articles or else I will delete their comments. I’m tired of having to waste my time rewriting the articles into the comments because people don’t read the articles.

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

The relative size of the balance sheet can be seen when total assets are figured as a percent of GDP:

This is all standard stuff having shown up many times in my articles.

i wonder what you call the 30+ trillion in national debt, which is increasing by trillions more every quarter?

not to ‘excuse’ the fed, but lets be real here.. they *SHOULD NOT* be the main target of your apparent disgust..

congress ‘spends’ the money the people DONT have, and the treasury sells the bonds to cover the deficiency.. to WHOMEVER:

including ‘ordinary american people’ looking for a return on their $$.

so you see, perhaps your initial finger-pointing is a bit misconstrued.

‘the ordinary american people’ must tire enough of congress’s reckless spending and stop funding a reckless gov’t debt addiction.

that has about a less than 1% chance of happening, IMO.

so, do you see the cycle now?

The Fed’s swollen balance sheet and lender-of-last-resort functions dictate that heroic CB interventions effectively enable chronic deficits. Left un-capped, monetary and fiscal intervention becomes an addiction, and any present removal of stimulus carries risk of ever-worse fallout than before.

Managed money interventions have worked to an extent, but the longer it goes on, the worse the future catastrophe when its un-sustainability is finally recognized, or forced. IMHO.

Also, QE and MBS therapy were both pretty huge misses on Fed management’s part, and a boon to federal and administrative money-spenders. That the public is appalled and seeks change seems logical.

What makes the Fed think that a 5.5% short term rate is restrictive enough to tackle inflation within a reasonable timeframe? Stocks and RE are moving up nicely and are at all-time highs. Doesn’t this lead to increased consumer spending and inflation.

If one is in the top 50% of wealth and owns stocks and RE that are advancing $100k per year or more, and the mortgage payment is fixed, why shouldn’t such a person increase their spending significantly? The ST interest rate doesn’t impact them one bit, not does it impact the vast majority of employers who have little debt or have fixed financing. A 5.5% ST rate might curtail the spending and hiring of zombies (both individuals and companies), but the zombies are a small portion of the economy and never had much economic influence to begin with.

It’s obvious to me the forces of higher asset prices, locked-in fixed rate debt and mortgages, deficit spending, the sight of QE in the toolbox, etc. make the 5.5% ST rate a rather weak and unreliable means to tackle inflation. Why have we paused here?

If the goal is to get inflation down in a more reasonable time frame of 0-3 years, 5.5% is not nearly restrictive enough IMO.

It’s like driving a car in snowy conditions. If you don’t make a big enough correction when the wheels give way, you spin out and wind up in the ditch. Make too big of a correction, at least you can fishtail around the correct path. The Fed should be erring on the side of reducing inflation, not risking decades of higher inflation.

Bobber, ‘erring on the side’ of deflation risks a self-reinforcing destructive cycle. We’ve seen decades of Japan’s central bank struggling to get out of its deflationary environment.

‘erring on the side’ of inflation doesn’t have the same kind of tipping point where inflation suddenly becomes drastically more self-reinforcing.

In your example of a snowy road, the better metaphor is trying to park on an icy hill: if you drive too fast, you risk driving past your parking spot and you have to walk further. If you drive too slow, you risk slipping backwards faster and faster, making it ever more difficult to stop before you reach the bottom of the hill.

The fed has significantly reduced inflation without sending GDP into contraction thusfar. After a huge increase (and subsequent taper) in the money supply, nonetheless. We still have people producing and spending, we still have dynamism in the economy. There haven’t been mass bankruptcies even with the largest rate increase in decades.

That said, ISM services went into contraction, which is interesting. The permabear in me sees auto inventories rising as another sign of an impending contraction. Hard to imagine we didn’t overbuild capacity with all that cash injection and stimulatory spending. But we sit at 3.9% unemployment. Best case is more steady as she goes with QT, maybe even a rate cut or two, and we keep consuming like the drunkin sailors we are.

“…sees auto inventories rising as another sign of an impending contraction.”

Actually, the inventory glut is causing the opposite effect: automakers are heaping incentives on their vehicles, and these incentives and plenty of choices have stimulated buying, and retail sales in units are up from a year ago. There is a lot of pent-up demand for cars; it’s just that prices gone up too far, but as soon as prices come down (=more incentives), sales go up… that’s what we’re seeing now.

Grant,

The whole point of the 2% target is to err on the side of inflation and address the risks you cite. The Fed should be comfortable taking inflation down to that level with some force and confidence because they have this 2% cushion.

This is simply not true.

If the FED focuses only on inflation and employment as they should, then Congress would be forced to face the effects of the debt they run up. Let the Federal government deal with increased interest costs.

I say this as a person who has no problem with Congress running modest deficits. Recent deficits are not modest.

So far the FED is doing that.

Bobber,

Stocks and real estate are not part of inflation. You are confusing/conflating bubbles with inflation.

They are different.

“That the public is appalled and seeks change seems logical.”

seeks change? where? name one single example of the public ‘seeking change’.

i believe i clearly said “not to excuse the fed”. so why does your reply contain a laundry list of fed transgressions?

i dont think you understood the point of my response:

the fed ISNT the only culprit, and should NOT be the sole object of the ‘disgust’ cited by ‘The original Marco’.

the are merely the facilitators of the financial debauchery practiced by the federal government, with the (indirect) support of the public.

JimL-

You say: “If the Fed focuses only on inflation and employment as they should…”

1. I know this has been discussed extensively in WS comments, but I can’t quite buy the proposition that elevated asset prices (like home and home prices) are NOT among the unintended consequences of loose monetary policy. [See:

https://www.federalreserve.gov/faqs/why-do-interest-rates-matter.htm

for a brief discussion]

2. You left out the very important but usually overlooked 3rd remit of the Fed: to promote moderate interest rates. The monetary lever-pullers sure botched that one over the last 20 years — ZIRP may be unprecedented, but it’s sure NOT “moderate.”

Perhaps that 3rd mandate is ignored because “moderate” has neither been defined nor limited. At any rate (gratuitous pun intended), whether policy rates should be raised or lowered is one of the lightening rods of most Fed discussions…

NoBoDy-

I should have acknowledged your statements that “the fed ISNT the only culprit,” “should NOT be the sole object of the disgust” and “they are merely the facilitators.” You are right, IMHO, that there is plenty of institutional blame to go around. But the Fed has played the dreary role as financial facilitator to out-of-control federal spending and bond price disruption…

As far as examples of seeking change, I refer to the “end-the-Fed” movement (proponents of which show up regularly in these comments) and the bitcoin phenomenon as exhibits A and B. I’m not a proponent of either, and neither represents a majority of the public… but neither can be ignored. The public is trying to discover “good money” (Hayek), or at least to change the system so that the value of one’s savings is durable and not subject to degradation. Other examples include the Mises Institute which has been seeking change for half a decade. Or Judy Shelton (nominated for Board of Governors of FRB), or the Lehrman Institute.

More names available upon request!

Respectfully.

NoBoDy-

…almost forgot one of the most vocal and respected proponents of change — James Grant — who has been writing on money and banking since the 1980’s. His congressional testimony is worth listening to, and his books are educational and entertaining.

Oops… In my above reply to NoBoDy, Mises has been a Fed-critic for half a century, not “half a decade”

@ John H –

a lot said with few words. Bravo.

The FED management also picked winners and losers and bailed out elites, bankers and wall street, which is their charter at least for the banks – the right banks.

grant said: “‘erring on the side’ of inflation doesn’t have the same kind of tipping point where inflation suddenly becomes drastically more self-reinforcing.”

——————————-

Weimar Germany? Zimbabwe? Argentina? current asset prices?etc.?

Many people I know currently spend more than they otherwise would because they don’t deem that foregoing the luxury today is worth the risk of holding worth-less dollars tomorrow. They would prefer to save but have no confidence in the dollar retaining purchasing power.

n0b0dy said: “the are merely the facilitators of the financial debauchery practiced by the federal government, with the (indirect) support of the public.”

—————————————-

the FED are also facilitors of the financial debauchery practiced by the bankers and exists to bail them out, at the expense of the lesser class.

The Fed shouldn’t be allowed to buy assets. Deposit money there only and have it backed by the money printer and not a bond that the Fed has to back it due to self-imposed accounting principals. And of course exist to set rates. And that should be their extent. But I guess Congress/Treasury want someone to buy their IOUs so here we are. More inflation that keeps compounding it’s no wonder asset prices keep going up.

Amen!

Z33-

“And of course exist to set rates. And that should be their extent.”

Wow. Why is the Fed in the price-fixing business? Are individuals, professional money managers, banks, bond traders, brokerage houses, corporations, foundations, foreign investors, pension fund managers, and municipalities incapable of discovering the market interest rate on their own? Does the government somehow knows the real price of money (represented by the rate of interest) better than the voluntary agreement of debt buyers and debt sellers on individual transactions?

It’s thinking like this that has gotten us into the dangerously unstable situation that we see today.

(Apologies for rant if you were being sarcastic and I missed it…)

Completely agree. Inflation, caused by reckless money printing, is another form of tax.

Treasury purchases must be very limited and FED should have never ever bought MBS. Buying MBS did no benefit other than skyrocketing housing prices.

Now MBS is rolling off. Even if they rolled of 35B per month (has been never reached in QT2), it will take 7 years for MBS go to zero. With the current pace of 15B per month it will take more than twice as much. Like a joke.

Thanks for the nice and clear analysis

Regarding QT, there is only one thing to say: Too little, too late. Now it will go down even slower. Reducing the pace of QT is a big mistake. It will fuel the bulls (again) and backfire with persistent inflation

Does the fed’s holding of MBS have much of an effect on real estate prices?

Alex,

I believe the Fed is having a profound impact on the Housing market. Think about unnatural effects on supply and demand by having a gigantic buyer of MBS and how that has driven the bond/mortgage rates to the low levels.

Without the Fed not buying MBS the mortgage rates are closer to reality.

This level has placed sellers and buyers into two camps:

1) Those who have a low mortgage rate and don’t want to sell and cash out their COVID-19-created home equity only to have to put that realized gain into another overpriced home only with a higher rate.

2) Those that can’t afford the higher home prices in conjunction with new market mortgage rates.

I feel there are three outcomes that cause the market to start flowing:

1) The Fed begins buying MBS again and the rates fall due to their influence on demand.

2) The economy tanks and we see a rapid drop in home values as people need to sell due to a drop in household income.

3) The wages catch up with inflation and people are able to adjust to the inflated home values and mortgage rates.

So, yes. The FED has an I oaft on the housing market and has created a bottleneck in the housing market.

Others may feel differently and I welcome their thoughts.

There is at least one other camp:

those who bought their homes over ten years ago when the rates were in the ~3-4% range, haven’t moved, and aren’t interested in moving.

They have equity also, but they can stomach a much more severe housing downturn and still sell at a profit if they need to than folks who bought in the last three years.

Great point. Thank you.

What is a MBS? A Mortgage Backed Security.

The thing that caused the GFC?

Pancho and JoeS,

Does the Federal Reserve need to buy them? Maybe they are toxic garbage like they were in 2008? Buyer of last resort, allow smooth functioning of the market, blah, blah, blah.

The Fed has reduced the “pandemic” purchases of MBS by 27%. Yippee skippy. Does the remaining 73% reduction bring affordable housing again? Or price discovery? Or disaster?

If it is disaster we should have let it happen years ago.

Rip the bandaid off.

Balance the budget or you’re fired.

Fed target for inflation is “0”. Or you’re fired.

My 2¢.

“Maybe they are toxic garbage like they were in 2008?”

Nonsense. The MBS that the Fed holds are government-guaranteed securities. For the Fed, there is zero credit risk.

“Maybe they are toxic garbage like they were in 2008?”

Nonsense. The MBS that the Fed holds are government-guaranteed securities. For the Fed, there is zero credit risk.

——————————–

You are correct Wolf. They are only toxic garbage for the taxpayer.

(and so goes the incentive to keep housing prices up with the resultant effect of continuing ongoing and future debt slavery)

So far, the post-financial crisis MBS have not shown any problems, with foreclosures still near historic lows. It would require a steep drop in home prices before losses will hit the taxpayers.

Joes,

I agree. I think the Fed is targeting 3 and a milder version of 2.

1) Income and wealth disparity is a problem. Before we become a third world country with the wealthy living in guarded enclaves and the poor dying down by the river, this needs to be fixed. Increasing wages fixes this for the masses. This may cause more inflation if wages go up causing prices to go up and the masses spend instead of save. Employers now automatically enroll new employees in a 401K to alleviate this and force savings. If the drunken sailors stop spending so much, corporate incomes will lessen causing higher unemployment which will lessen inflation.

2) Housing prices have increased 30-40% which FAR exceeds CPI inflation or dollar devaluation. This has been caused by FED interest rate suppression and MBS purchases. It is a housing bubble. Selectively deflating it 20-30% will help bring housing price appreciation back to the inflation rate. I believe that if the depreciation drops more than 30%, panic will ensue and prices will drop more than 50%. It is a delicate job to avoid another GFC and drastic housing crash.

I am waiting for Wolf’s famous Case Schiller house prices and rent prices chart to intersect again like they did in 2012. Primary home prices and rent prices should track inflation. They did from 1950-2000 before all of these bubbles appears.

The problem is that is a certain percentage of the country that continues to vote against their best interests because they are too fearful to do otherwise.

Want to reduce wealth inequality? Eliminate health concerns. The U.S. is thr only first world country where an otherwise mildly wealthy individual can go bankrupt due to a simple health problem like breast cancer. Yet there is a certain segment of the population who continues to vote against any health care reforms due to “socialism”.

Stupid.

Bob E said: “Employers now automatically enroll new employees in a 401K to alleviate this and force savings.”

——————————–

This has been great for diving passive index investing, the stock market and assisting in sustaining Zombie companies. Wonder how that continues to go ……….

cb, you are correct.

Blindly adding to 401K funds that invest in funds containing zombies is counterproductive. Over the long term, stocks have yielded 8%. Much better than long term bonds or anything else.

My 401K includes bond funds and I followed the 40% recommendation to my detriment for the last 5 years thanks to the Fed’s irresponsible rate cuts.

However, now my bonds outperform stocks with fixed income.

This is all a game. I’ll cash in my bond funds (or not) and my mortgage when it makes sense (ie stocks plummet 50% like 2008 and mortgage rates drop below my savings rates). For now, this isn’t happening so I continue to hold my balances. This is called diversification. I believe in it for the long term even though I may be wrong in the moment for some of it.

My crystal ball broke in the 1994 Northridge quake so I have been diversifying and hedging ever since. This is why I need Wolf’s excellent advice to try to read the future. I cannot predict the next big bubble where I invest 10K and walk away with billions. Wolf doesn’t even try to predict insanity. There are too many insane people out there trying to sell me their ideas and 99% of them are wrong.

Employees only start contributing to their 401k target date fund from this secure act thing if they take no action. They are not forced, but many either trust their employer or don’t want to do the relatively simple steps of stopping the contributions. Some 401ks dont have money market funds and the problem is that stock indexes are very overvalued now so the employees are unknowingly overpaying for these assets and stocks could fall by a lot or go “on a long strange trip to nowhere”. The bond funds they’re buying have already fallen substantially so they’re a better deal but rates could also still go higher. I think this secure act 401k thing was created by tptb to purposefully support asset prices.

I see that your “lowest guess” for the lowest possible level of the Fed’s balance sheet in 2026 was $5.8 trillion. This estimate of getting to $6.63 trillion by the end of May 2025 would mean $830 billion for the 19 months between May 2025 and December 2026, so “just” $44 billion a month. That seems doable. I’m hopeful that the Fed just might execute QT better than expected 2 years ago!

Id like to see a graphic that extends the Assets line down thru May 2025 over a Liabilities chart similarly extrapolated.

My sense of it is that deceleration of QT will eventually result in a much higher intersect point with liabilities in the future.

The asset chart and the liability chart look just about exactly the same. The only difference is $40 billion in capital, which is a constant.

I can clearly see you are displeased with some of the comments calling for more QT not less, but when considering this plot, what is a good rate to get back to pre 2008 levels? The Fed seems to be playing a balancing act to keep asset values high and not inflict any economic pain at all aside from inflation. The logic goes as long as the value of equities and housing prices increase higher than inflation, it’s all good.

Nicholas Rains

“… to get back to pre 2008 levels?”

People who say that the balance sheet should be at $800 billion now to get us back to where we were don’t understand what the Fed’s “balance sheet” is and how it works. So let me help you with this.

In 1976, the balance sheet was about $100 billion. And it grew steadily to $900 billion by 2008, before QE started, so that’s an 800% increase.

In the five years between Jan 2003 through Aug 2008 (before QE), the Fed’s balance sheet grew by 27%, from $712 billion to $910 billion.

It increased dollar for dollar with currency in circulation (paper dollars), which are a liability for the Fed, and must be balanced by assets for the balance sheet to balance. During that time, relatively speaking, the balance sheet remained at about 6% of GDP. Currency in circulation is demand-based: Those $20-bills must be in the ATM and at the bank branch when you’re trying to withdraw them. The Fed provides currency to the banks and they must have it ready for their customers. Maybe half of USD currency is overseas, for various reasons, which is where a lot of demand for it comes from.

Since 2008, the balance sheet must grow not only with currency in circulation but also with the TGA. This is the government’s checking account that was moved from JPM and other banks to the New York Fed during the financial crisis and has therefore been on the balance sheet since then. Both currency in circulation and the TGA are a liability for the Fed, and assets MUST balance liabilities dollar for dollar when capital is fixed — which the Fed’s capital is — so that the balance sheet balances.

READ THIS – it discusses currency in circulation and the TGA, along with the other big liabilities on the Fed’s balance sheet:

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

Here’s GDP, not adjusted for inflation. The Fed’s balance sheet is also not adjusted for inflation:

The relative size of the balance sheet can be seen when total assets are figured as a percent of GDP:

The problem we had were the two phases of QE (2008-2014 and 2020-2022).

It should have NEVER bought any MBS ever. It should have never done QE with bond purchases. It should have used repos to deal with market problems (GFC and pandemic), as it used to do before 2008. That would have worked fine. Those repos would be gone after a couple of months, as markets go back to normal. That’s what it did during 9/11, as markets were actually shut down for a few days, and chaos ensued, and it doused the markets with liquidity via repos for a few days, and after a couple of months, the repos were gone, and the dotcom bust continued.

Financial Crisis QE is ancient history. 2008 was 15 years ago. Pandemic QE was years ago. Whatever it did, it did. Water under the bridge. Now we have QT, the biggest ever, $1.6 trillion so far, and people are blaming the Fed for QT. The Fed is finally and for once doing the right thing. The enemy is 0% and QE, not 5.5% and QT.

Wolf-

You accurately state that: “The only difference is $40 billion in capital, which is a constant.”

Had I composed that sentence, I would have added the word “embarrassment” at the end…

Thanks for continuing to illuminate the murky!

The Fed is compelled by law to remit all its profits to the US Treasury Dept. Its capital capped by law. It’s in a 100% tax bracket, so to speak, and can never accumulate capital. All excess capital is remitted to the Treasury Dept.

How is it that FRB capital is limited by law but the balance sheet is not limited by law. Doesn’t capital usually backup a firm’s ability to pay it’s obligations?

Is there no limit to the size of the Fed’s other balance sheet components? Should there be a limit, especially given its privileged position having a monopoly on base money production?

I’m sorry if I missed it in one of your articles, but would you be able to explain the Fed’s thinking during the “no crisis” section of their balance sheet expansion?

I was still pretty young at the time, but I remember the GFC recovery being well under way by the beginning of 2013 and the 40ish% increase in the Fed’s total liabilities just seems like it was so unnecessary.

“…would you be able to explain the Fed’s thinking during the “no crisis” section of their balance sheet expansion?”

It’s inexplicable.

Wolf,

FED has shown resolve to do QT for last 18 months. Many had doubts and FED displayed their resolve in Action. Good job in fixing part QE mess it got created.

I agree that they should slow down at certain point so that they can go further in terms of reducing the balance sheet.

We have 400B+ in ON RRP, Reserves have 3.3T and they have opened SRF.

My question: Do you agree or disagree they slowed down QT process too early?

Shouldn’t they wait till at least ON RRP comes to near zero or 100B at least.

I am sure they can go 4-6 months before slowing down.

Here is my humble opinion as a FED moderate.

Personally I think the FED is starting to taper QT a little bit too early. I think they could go a bit longer. Q3 OR Q4 at the very least.

That said, I also think it is far better to start tapering QT too early rather than too late. It is like pulling into a parking spot that has a concrete wall in front of it, better to slow too early and ease forward rather than slow too late.

Again, if I was God, I would have had the wait at least a meeting or two before tapering, but I understand the reluctantace to hit the concrete wall so to speak.

Here’s another analogy: its like pulling a shipping label sticker off a box so you can reuse it.

If you try to pull the label off too quickly, it will just tear, leave residue behind, and never come off cleanly. But if you peel it off reeeeally slowly and gently, applying a little heat as you go, the label will come off completely and in one piece.

“Slow & steady wis the race” being the guiding principle here.

2 two are a couple of loony birds, one of you is God, the other is pealing the label off a can of noodles.

I say this as a bird lover.

From the article,

“After months of talking about it, the fed has clarified officially when, how, and by how much they will slow QT”

Is this official announcement going to change next week or next month? And what would God do?.

Home Toad,

Your failure at comprehension dies down mean that we are gods or are loony. It just means you failed at basic comprehension.

If you need help, ask specific questions and I will try and help.

JimL,

What will happen if the Fed continually errs on the side of inflation in its attempt to avoid hitting the wall?

Please put a goal post in the ground and tell us when, in your mind, inflation should be back to 2%. If the Fed doesn’t meet your expectation, we can remind of it.

Easy question. You should already know why.

The FED should try and get back to 2% inflation ASAP without being responsible for putting the economy into a recession.

Remember, I firmly believe that the FED cannot completely control inflation. I think they can pressure it, but it isn’t a simple dial where they can turn it to whatever they want. It is stupidly naive to think it works that way.

I genuinely believe that inflation will not go to 2% or below until there is a recession. It won’t.

However, that does not mean that the FED should automatically throw the economy into recession. The can continue to put pressure on inflation and keep it as low as possible for as long as possible.

For the record, I am on record here of thinking the FED will have to raise rates. Admititly I think it is close, but I would be fine with a rate increase.

It should also be noted that there is a distinct difference between interest rates and QT. They affect different things. QT is more about asset prices which are slightly different that actual inflation (though very closely related).

JimL,

Hussman has done great work indicating the best indicator of future inflation is past inflation. I believe not getting back to 2% inflation in a reasonable timeframe, say 0-3 years, will have severe negative consequences. It would kick of a feedback cycle where inflation and LT interest rates rise, causing a larger recession down the road.

We disagree on the recession issue. I think the Fed should act diligently to achieve it’s 2% target now, even if that means recession. Better to accept a smaller recession now than a larger one down the road. This would also mitigate wealth gaps and generational fairness issues.

Take the medicine now, I say.

The Fed owns a limited amount of Treasury Bills, which are an important part of their strategy. Reducing QT allows the Bills currently on hand to fulfill their QT role for longer.

If the Fed wants to get rid of MBS, why would there be a monthly cap? If there are $100 billion mortgage payoff in a month, so what? More than likely there’s a similar amount of MBS created somewhere else because of churn. Why would the Fed buy more treasuries or notes to replace the MBS above $35 billion? I assume it has to do with its liabilities?

MBS are unpredictable, and the runoff represents a liquidity withdrawal from the financial system. Withdrawing liquidity can get dicey. You’re yanking money away from economic entities that had relied on it being there. They can adjust, but it can take some time to adjust. So the Fed put caps on the roll-offs. Maybe it’s not necessary. but they’re trying to keep everything predictable, and they’re trying to make sure nothing blows up.

Wolf,

Assuming the housing market stays frozen, is there any scenario where MBS rolloff could or would run above the cap?

If home sales stay this low and refis don’t increase, the MBS runoff will stay in the range it is now, that’s my guess.

I think the cap on MBS is there simply because no one knows what is appropriate without causing liquidity problems in the system.

The cap hasn’t been reached yet so it is all theoretical anyway. No one literally knows how much MBS they can allow to roll off without breaking anything.

Maybe the FED can hit the cap a few months in a row and recognize that no cap is needed. Maybe they will hit the cap and some things will start to look dicey.

Until it happens, no one knows so the cap is just there to not let things get too crazy.

I wonder what the median and average maturity dates are for all of the MBS’s the Fed holds? it has to be less than 30 years. Less than 28 years now.

My guess that with all of the refi’s, it is closer to 15 years.

Anecdotally, most people who refi’d that I know, refi’d at 15 years or less at a rate of 2.5% or less. I know mostly GenX or Millennials in their 40’s and 50’s who didn’t want a mortgage when they were 70 or 80.

At 3% or less, the yearly principal passthrough payments are large and are growing larger every year.

Combined with deaths, divorces, and disasters, the slope of payoffs should increase naturally and the balance should drop at a higher rate between the next 13 to 25 years. Considering it has been 16 years since 2008, the start of the last housing bubble, this isn’t that long.

@ Wolf – “You’re yanking money away from economic entities that had relied on it being there.”

———————————————

Who are yanking the money away from?

The entity paying down the MBS voluntarily does so and apparently has the capacity.

Less money in the system seems a good thing. It puts downward pressure on home prices. Unfortunately, more loans and purchasing dollars can be created so that downward pricing pressure can be offset.

“You’re yanking money away from economic entities that had relied on it being there.”

What that means is that companies run out of money to meet payroll when liquidity that they’d relied on dries up. This happened to lots of startups and bigger companies with thousands of employees, when SVB collapsed and they couldn’t get to their cash in the bank to meet payroll. That was a classic case of liquidity not being there that companies had relied on being there. The depositor bailout averted a potentially rough situation for these companies. Liquidity is not a toy.

Continuing MBS runoff could keep mortgage rates where they are now unless the Fed substantially reduces interest rates.

Will the slow down in QT and possibly adding additional treasury securities through making up excess MBS rolloff have the effect of depressing rates because otherwise the treasury would have to be selling more in the open market to make up for the unreduced roll off? This is this a signal the Fed does not want to see treasury interest rates increased?

No, none of the above. They’re still WITHDRAWING liquidity, just at a slower pace.

What a bloated, disgusting mess. The pace of QT is WAY too slow. Just look at the Canadian central bank. They have unwound things much faster.

None of this QE was even necessary, so they could drain it much quicker than they are. Instead, they’re going to punish the working class and the poor for as long as possible, dragging inflation out for years.

There is a reason Canada could unwind QE much faster. They are not the economy the whole world relies on. How many loonies do you have stuffed under your mattress?

I know your response will be “who cares about the rest of the world?”

If that is true and the rest of the world starts suffering, do you think it will also affect the U.S. economy?

Ahh, right, I forget, you are pro-pain. You want to see suffering.

JimL,

It’s a rip the band-aid off vs picking at it slowly. The slow pickers are not good decision makers.

What is your estimate based on? Besides, what does your analogy have to do with the fact that the U.S. economy is far more important due to it’s size and complexity that the Canadian economy is? That is an absolute fact.

The FED has caused its’ share of suffering, and subjugation. And for some, elation.

There was a Pandemic after all….empty streets and a crashed economy. Although some dispute the more than 1 million US deaths, even today. QE was necessary. QT is necessary.

Positive story and easy to understand line graphs of the trend. Thanks.

It’s hard to imagine the counter-factual: what could have happened if the Fed didn’t do what it did. Where would you and I be, in what condition? No one here can answer that (as in 2008 also) provably. Maybe the Fed over-did, but this is not an exact science, because again, there is not a laboratory condition where the situation can be replicated. It is like steering 500 irregularly-shaped-and-sized aircraft carriers at once: the axes of a world economy. But we can see events in the 1800s and 1900s where financial collapses brought years of hardship (nobody here has seen anything like it) and even global war. THAT (real history) is my baseline for considering what is reasonable to expect. Talk in a setting like this is, in a sense, cheap (though I do appreciate everyone’s two bits). I have a job and reasonable dollars and financial system, all of which is underrated.

I have a pretty guess what would have happened if the Fed didn’t do QE during the pandemic. The government would not have been able to spend so much, and demand would have dropped to meet the reduced supply.

Asset prices would have dropped temporarily, but they would have returned to NORMAL levels once the pandemic was over.

Employment would have suffered a downturn, but like asset prices, employment would have returned to normal after the pandemic. Unemployment compensation would kept the unemployed afloat until normal employment returned.

It’s because of QE that we saw a 20% inflationary step up, excessive asset price growth, and breakdown of trust in the system.

They didn’t need QE. I think extended unemployment benefits, the vaccine, and modest reductions to interest rates would have done the job.

We have more than a hundred years of history pre Fed to show us what this looks like.

There were frequent panics and recessions prior to the existence of the Fed, but very little inflation.

There are still frequent panics and recessions post Fed, and one Great Depression, which the Fed worsened with tight monetary policy.

The trope that “it could have been worse” is a pile of crap. No one knows. You can’t prove a negative.

But we can see the enormous damage the Fed has done post 2008 with massive distortions in assets and now raging inflation post 2021. We don’t need the Fed. We need sound money.

Happy1,

That is simply not true. None of what you posited. It is as false as your claim that the U.S. should territorially claim the moon. Silly.

Why is it that every first world country (and most 2nd and 3rd world countries) have a central bank?

Until you can answer this you are flailing.

@JimL

Territorially claim the moon? Not following…

As to the veracity of what I posited, all of it is verified historical fact. CPI inflation from 1800 to 1916 was 0.4% annually, and has been 3.5% annually since, this is per the Fed’s own St Louis branch and verifiable with a simple Google search.

Remember that until the 1970s, the Fed’s sole mandate was price stability. The phrase “you had one job” comes to mind.

GDP growth was also substantially higher pre Fed and also higher prior to Nixon uncoupling the dollar completely from Gold.

If we are worse off with Fed managing the economy, with more inflation, massive asset missalocation, and massive income inequality relating to assets being inflated, a reasonable person can and probably should conclude that the Fed is part of the problem and a return to sound money is what we need.

You can hate facts as much as you like, but it doesn’t make them not facts.

True. The FED helped avoided a recession. Foreclosures. …etc

Now they were able to tame rapid inflation with QT while keeping the economy humming a long with low unemployment. (Lots of experts were calling for a recession to happen at the beginning of 2024).

Sure, some assets are overvalued but people have jobs. 65% of the people own homes. We will always see the stories of people living paycheck to paycheck.

The FED would rather have people complaining about slightly high inflation than lined up at soup kitchens.

Long term rates in Canada are about 4/5 of a percentage point lower than in America. QT didn’t drive long term rates much higher in Canada.

Good News!! Good News! Roscoe – “At current rates, the U.S. national debt is growing by a remarkable $1 trillion about every 100 days, equal to roughly $3.6 trillion per year.”

The richest most powerful country in the world, who cannot control its own borders or budget. The chinks in the Armour are starting to show. Reactive Leadership digging a deeper hole to the abyss. I’m staying in my foxhole, the FED has silenced lynch mob on Wall St. while Janet Yellen screams outrage that Gen Z cannot afford to buy home right now. Californianians boycott McDonald’s prices, while Applebees closes. U can’t make this shit up.

Studio apartments start around $500,000 in most of Canada by population so GenZ and all others are shut out of the housing market indefinitely.

The issue is that renting is terrible too. House hoarders demanding C$1,000 a month to share a room with several international students like a prison cell.

Even high priced rent is being charged to share a bed with a stranger.

/sarc

Well….those are some issues that will eventually have to be addressed. But right foreign policy and foreign aid is more important.

I have a pretty good guess at where you get your information. In fact I would bet a lot of money on it. Literally tens of thousands.

Get better sources of information. Ones that inform you rather than scare you.

why do you want to screw up RU82’s story?

“It’s an institution of the United States, set up by Congress”.

Partially true. Like any other piece of legislation, Congress did not write the law or set it up. The bankers created the template, drafted the language, and Congress enacted it into law.

That aside, I guess I’m in the FED ‘moderate’ camp with you. The bigger problem, IMO, is a Congress that refuses to do their job. I can’t find the video where Powell tries to explain why the inflation target is 2%, but it’s a word salad from a bad lawyer. And yet, not a single follow up question of where 2% came from (an Australian TV interview years ago), why it’s not 1% or 3% or zero. There might be a dozen members of Congress who understand the US economy. And that is the real problem.

Simply: It’s 2% because that’s about as low a target as it can be where normal variance does not go negative. Deflation is BAD so they picked a number where they had high confidence they could step in and correct it before such happened.

No, INFLATION is BAD. What we need is massive DEFLATION.

Obviously you do not understand what deflation entails. Embedded inflation is bad. No doubt. Embeddd deflation is much worse. Not even close.

Deflation is not bad. Deflation in goods at least isn’t bad. Things should be cheaper over time as efficiencies come into play. Or up front costs are amortized. Somehow the 25% deflation in flat panel TVs per year (size and technology) hasn’t ended the flat panel TV market – it just makes people upgrade more. 4k, soon 8k, etc.

1-5% deflation in goods isn’t going to keep anyone from buying what they need now. “Johnny, you know if you just keep wearing those size 8s for another year this time next year those size 10s will be cheaper “. Absurd.

For services I can see targeting+2% inflation. People are valuable, their time is valuable. So -2% in goods and 2% in services. Make me Fed chair for a day..

Your statement is both absolutely true and naive at the same time. You need to account for productivity as well as inflation when calculating the cost of TVs. Economy wide deflation is absolutely horrible.

Imagine every year going in for your annual review and find out your pay is being decreased. Also, in economics, group outlook has an effect. If people think the future is brighter they will spend, if they think it is bad they will save.

In a deflationary environment, it is always smarter to delay purchases as long as possible. Things will be cheaper tomorrow. Why not wait? Smart.

Now imagine what happens to economic activity when everyone waits to purchase stuff? What percentage of businesses or going to be gone?

JimL

Deflation is most certainly good after this past few years of out of control inflation. We need to unwind the damage, especially housing, that was done since 2019. And your post is about why deflation is bad for spending. That’s the problem with this country – SPENDING and wall street’s never ending quest for more and more. You sound like a textbook written by someone who works on wall street. Tired of your posts.

Thinking that “deflation will unwind the damage of inflation” is as foolish as thinking you can un-burn burnt toast by putting it in the freezer.

Partially true? No, it’s entirely true. The Federal Reserve Act is an act of Congress signed by the President. How the legislation was drafted and/or its contents debated in Congress does not matter, it is still an act of Congress which authorized the creation of the Federal Reserve System in its current format. In this regard, Congress alone can amend or repeal the act as it sees fit.

Point to me where the charter of the Federal Reserve allows asset purchases. It doesn’t. They didn’t ask permission, they just did it. And they clearly have no way to reverse it.

Where does it say they can’t?

I am not defending asset purchases by the FED. I didn’t like them. Calling they illegal us different though. Back up your arguments with evidence, not emotion.

What does your comment have to do with my comment? Nothing. I was pointing out the entire Federal Reserve System was created by an act of Congress. If you do not believe the law as enacted by Congress is being adhered to, you should contact your representatives. Congress can take action if it does not believe the law is being followed.

Furthermore, the Fed has always purchased assets since assets must equal liabilities plus capital on the Fed’s balance sheet. I suspect your issue is with QE, but I don’t want to speculate.

@rojogrande

Yes I was referencing large scale purchases of long term bonds and MBS.

The Fed charter is not a document that allows them to do anything they want in achieving their dual mandate of price stability and maximum employment. There was pretty significant internal controversy when they initiated QE as to whether this was legal, they get away with mission creep like this whenever there is a crisis, and Congress is happy to see someone else take both the risk and the blame so they can spend time grandstanding and fundraising instead of you know, the hard work of legislating. Which is their only job.

Remember, per the 10th Amendment, “powers not delegated to the federal government by the Constitution are reserved for the states or the people”. The Fed can’t simply conjure up whatever they like, such as buying US stocks, or giving money to a specific business or individual, that’s not the way it works. I agree that Congress is also at fault here and should delineate better Fed limits, but they have delegated their work to the administrative state. Illegally I would add.

It’s two percent to justify a continual wealth transfer to Congress by the hidden tax of money creation.

Thats the bargain the banksters made with the politicians: you give us control over the money supply, and we’ll ensure there is always a buyer of your debt to fund all the pork-barrel shenanigans your heart desires.

The “bla bla optimal inflation targets bla bla economic expansion bla bla” word salad is just the shuck they’ve been putting on the rubes to conceal the heart of the enterprise.

Youe nutty tinfoil hat conspiracies aside, it should be noted that there will always be buyers of government debt. Always.

It just matters at what interst rate it will be at. Interest rates solve all demand problems.

JimL-

What happens when “interest rate solve all problems,” but the Fed price-fixes interest rates for a decade or so?

Nothing good, we’re discovering…

The progress the Fed has made over four years is amazing in the big picture, and the majority of people have extremely short memories, forgetting or ignoring the unfolding global depression during March 2020:

Between Feb. 12 and March 23, the Dow lost 37% of its value. By the the middle of March, panic was rising.

Many may not like the current state of affairs, but all that excess stimulus literally saved the world from epic failure.

The global depression was government caused.

“but all that excess stimulus literally saved the world from epic failure.”

Another BS comment that should rank as one of the worst in the last five years.

Houses are C$1.5 million in Canada, rent is C$2,500 a month for a one-bedroom apartment, and there are very long lines for a minimum wage job in world-class Toronto.

The rich benefited wildly from ZIRP. The vulnerable disabled population in Canada are promised an extra C$200 a month which requires a doctor to sign a complex form costing about C$200 to complete out of pocket. Many choose medically assisted death instead because the cost of living is unbearable.

jeez Don’t kill yourself Move — Canada is paradise. In You are not chained to your location. there are many places in Canada and the US to live you “chose” to live in Toronto. We moved out of Ontario to Nova Scotia. there is a housing shortage here but you could try New Brunswick or Quebec and if you get out of the large cities you will find that Canada is really paradise. If you want to stay in Ontario northbay and the Sault cannot possibly be that expensive

My guess is that they will continue their current policies until the next “crisis”.

If (when) the the next recession hits, another “surprise” will present itself. Then the Fed continues its policies and once again moral hazard enters the picture with all of its ugly results.

Good luck Mr. Powell. I think we’ll need it.

Brewski,

You’re fantasizing and you’re abusing my site to spread a BS agenda. I have explained a million times why your comment is BS, and why it’s an agenda that’s being promoted in the social media.

If MBS are just going to be replaced with treasuries, why even have separate caps? It would be simpler to have a single combined QT cap of $60 billion.

That would permit treasury-only rolloffs to be up to $60b a month, which is too much for the fed’s plan.

It appears they’re not concerned about the MBS markets getting spooked/flooded, but they are cautious about the Treasuries markets getting spooked/flooded.

“The Fed lets them roll off (doesn’t replace them when they mature) only if not enough longer-term Treasury securities mature to get to the $60-billion monthly cap. This allowed the Fed shed about $60 billion in Treasury securities every month.”

Wolf, can you please explain in “layman” terms why reducing the amount of T-bills will or will not affect the T-bill rates in the future?

It wont affect T-bill rates. They are bracketed by the Fed’s five policy rates, and by market expectations of those five policy rates within the time window of those T-bills (i.e. a 3-month T-bill only says something about market expectations of Fed policy rates over the next 3 months).

It is great that in a comment Wolf cites Japan and they are “still doing QE”. It seems that the great problem of inlfation and paper money always ends up with some kind of monetary manouvering, when you don’t have a system which bases itself on responsability.

The Japan phenomenon is a warning sign, which showed that stock bubbles can get so big (at one point the Imperor’s palace area in Japan” was worth more than the entire California and the price of 1 square meter was 300.000 Deutch marks (around 150.000 EUR). Then everything imploded and ended in a deflationary mess that the Bank of Japan tried to fix with zero rates …

After the financial crisis of 2008, everything collapsed and the idea was the same: let’s just print money, bail everyone out and the modern monetary theory (which way bollocks!) was promoted that there can not be any inflation, because of the vastness of the collapse.

The idea that you can somehow artificially fix a collapsing bubble with printing money is nice, but in reallity you can not. So this is just agonizing … QE for 10 years, then QT, then the everything bubble will collapse, and we’ll be there again: QE all the way.

No one is willing to admit that there is something in the system that just allows greed to expand exponentially and there is no one to stop it, but instead of regulating this phenomenon and acting responsible, there are just blind people at the wheel, who simply don’t care as long as they make profits.

You can not have 35 trillion in debt and act everything si fine, and then pile up another 1 trillion every two quarters.

I hate the system/corruption with a passion. Wish it would collapse. I’m sick of everything wall street.

All of the MMT stuff was crazy to watch, and suddenly disappeared…I read a book called Price Wars which was about commodity prices but the author reveals himself to be an MMTer in the last chapter, saying it’s a “myth” that money printing causes inflation. Then inflation took off like right after that book was released and I was laughing. This really is the dumbest timeline.

The FED is literally doing the opposite of Japan. How can you say they are a warning sign?

The Imperial Palace In Tokyo was never for sale, would never be for sale, and so ridiculous measurements and statements like that should be put in the garbage bin.

Now wall street is rallying on the jobs report, expecting a rate cut any day now. Yields were tanking, haven’t looked in the last half hour. The system is rotten to the core.

Who gives a sht what estimates were. Tired of the entire game.

Why is the desert rats down?

It nothing more than a game board you’re a piece of. The dice are rigged, the board shifts, go back 3 spaces is often the card drawn? Go to jail.

Yes DR, now I see why you are down.

The Bank of Canada has reduced it’s entire balance sheet by 47% from peak. It’s understandable that some people are complaining that the Fed has only managed 17.8%; they will go even slower in June.

Yeah, but the Canadian dollar doesn’t really matter to global finance and the global economy. Not that many countries and companies borrow in Canadian dollars. If high rates and lots of QT cause the USD to surge against other currencies, all kinds of bad things are starting to happen, especially in developing economies with lots of dollar debts. The dollar needs to be managed carefully. There is a lot of responsibility on the Fed to do that smartly. I’m not sure the Fed is doing a good job managing the dollar, and I have my quibbles, but I can see that they’re trying.

Also the BOC may end QT before the Fed. It has already indicated when:

https://wolfstreet.com/2024/04/07/bank-of-canada-balance-sheet-qt-sheds-64-of-pandemic-qe-assets-indicates-qt-might-end-in-september-2025/

MW: Trump blames strong dollar for U.S. economy ‘going to hell’

People who listen to DJT for economic information deserve exactly what they get. They simply don’t realize it and will blame others.

I have heard the comment that the FED is not going as fast as Canada.

I always like to ask those people how many loonies they have under their matress.

Juncture recognition should involve the deflation of housing prices, not just a deceleration in R-gDp. QT tapering won’t accomplish that. Powell would have to continue with holding the money stock constant.

MW: The Dow 30 surges 400-plus points. Credit April’s payrolls report and Apple’s planned payout.

Wall Street seems to have forgotten that you “don’t fight the Fed.”

So many commentators thinking that they are more knowledgeable, smarter than Powell. Good luck with this attitude. How successful are they in other aspects of life?