- Search Forex Factory

- 351 Results

-

JeremyWS replied Apr 21, 2014

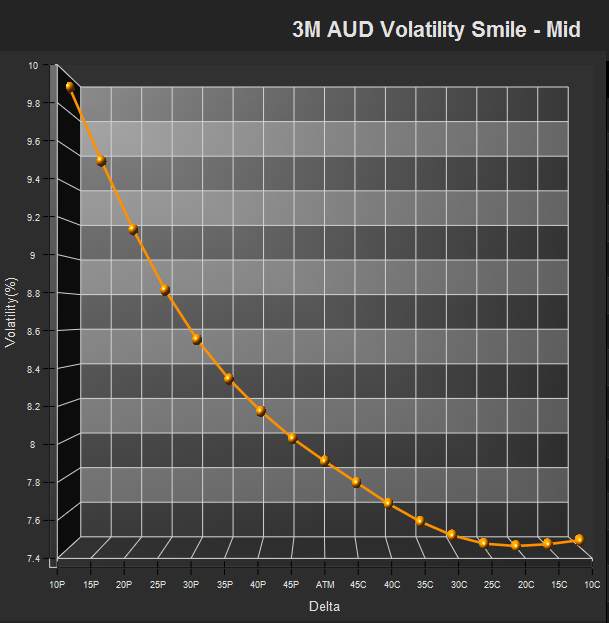

JeremyWS replied Apr 21, 2014well as said, the volatilty smile determines the relative vol to the upside and downside. Volatility for 1.60 strikes in GBPUSD will be far more expensive than 1.8 strikes, because the market knows the positioning is very long, and so a fall lower ...

EURUSD

- JeremyWS replied Apr 21, 2014

Should add, actual vol tends to be lower than implied vol as the market normally overpays to hedge. imagine you are a trader and you haven't hedged a position and there is a huge move, your risk manager is going to be very mad. so most tend to ...

EURUSD

- JeremyWS replied Apr 21, 2014

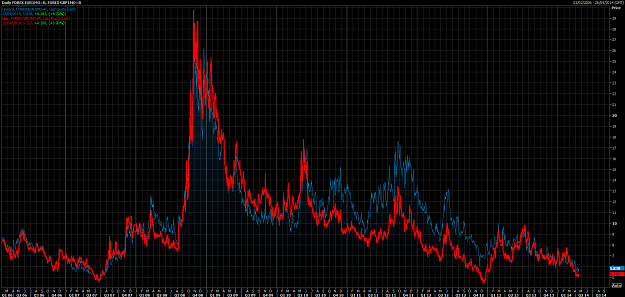

Implied/expected volatility is lower in GBPUSD than EURUSD, therefore you would expect a lower % move in either direction (depending to some extent on the volatility smile (colourful one) (both attached) But implied/realized is not always correct, ...

EURUSD

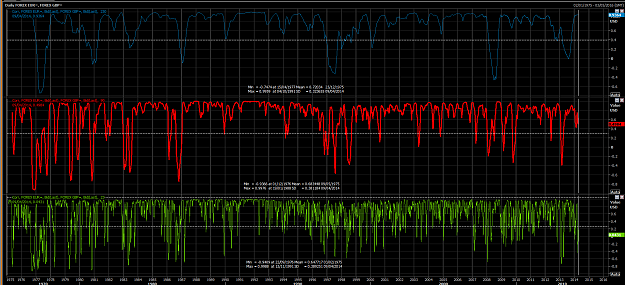

- JeremyWS replied Apr 21, 2014

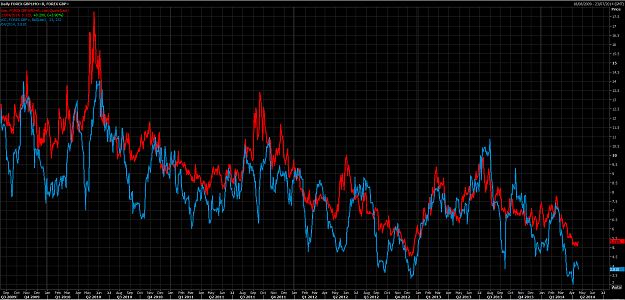

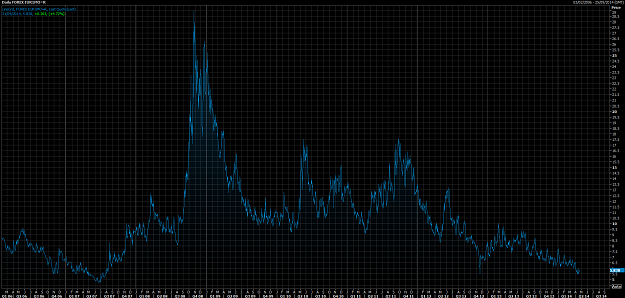

I don't know whether he used hist/realized vol or implied vol, but the standard way to risk-adjust your trades is to consider a forward looking implied volatility, typical swing trades might use 1 month IV (chart) We can see that its at 5.8, much ...

EURUSD

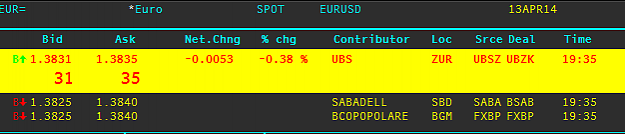

- JeremyWS replied Apr 20, 2014

fwiw, Dankse bank copanhagen office quoting EURUSD at 1.3809/11 so far, no gap this week. but there is no reason for one so...

EURUSD

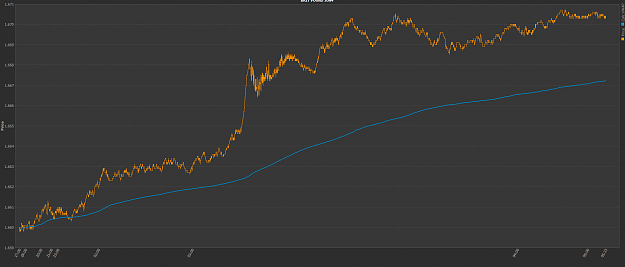

- JeremyWS replied Apr 20, 2014

yes, there is a period of volatility you are missing as shown below with the UST 6 month swap spread this should help with a basic understanding - url also this - url

EURUSD

- JeremyWS replied Apr 20, 2014

same picture as before, but normally one uses X-CCY BS' It would be better to consider the asset-swap spread / z-spread on the 6 month bubil

EURUSD

- JeremyWS replied Apr 20, 2014

what credit risk? there is none left it would seem just load up X-CCY basis swaps. never been tighter....

EURUSD

- JeremyWS replied Apr 20, 2014

The principal argument in QE/CE is to lower real yields. (nominal - inflation) So, this comes about in two ways, Higher inflation and lower yields. Given low yields already, a negative rate cut is barely anything on the margin, and therefore it can ...

EURUSD

- JeremyWS replied Apr 20, 2014

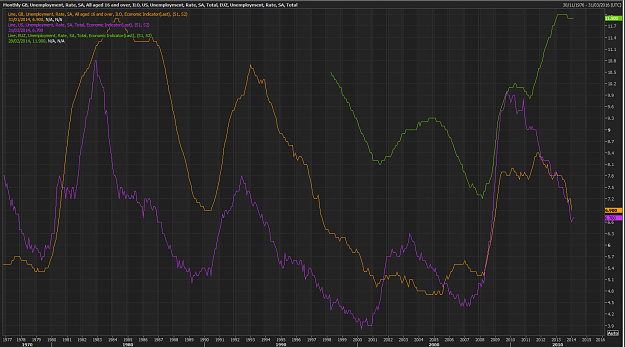

true - Low U/E in EZ is considered ~7%, which is considered uncomfortably high for the US/UK

EURUSD

- JeremyWS replied Apr 20, 2014

true, it comes from my experience. But EM is not G10. My time on an EM trading desk for top 5 EM bank leads to be fully believe what I say. Yes, technicals can work, and work reasonably well on EURUSD, or AUDUSD or whatever. but USDTRY/ZAR/THB/MYR ...

USD/TRY

- JeremyWS replied Apr 14, 2014

Swap rates change on an hourly basis. it is the market moving, not the broker

EUR/CHF

- JeremyWS replied Apr 13, 2014

no you are right... the Goldman sachs weekly FX open note citing Draghi as the reason is completely wrong and you are entirely right. Also, take note of USDJPY (if it was ukraine we'd be under 101 by now you fucknut)

EURUSD

- JeremyWS replied Apr 8, 2014

1 year rolling correlation - top 1 quarter rolling - middle 1 month rolling - bottom All data going back to 1975 as per Reuters. Mean over the period is about 0.7 or so

Cable Update (GBPUSD)

- JeremyWS replied Apr 8, 2014

The only thing that matters right now for every asset class EUR / FX Stocks Bonds Commodities They are all watching this line - it will set the tone for the entire financial markets for the next few sessions.

EURUSD

- JeremyWS replied Apr 8, 2014

Market very short gamma still, meaning its hard to get pullbacks, but first support is VWAP around 1.6670

Cable Update (GBPUSD)

- JeremyWS replied Apr 7, 2014

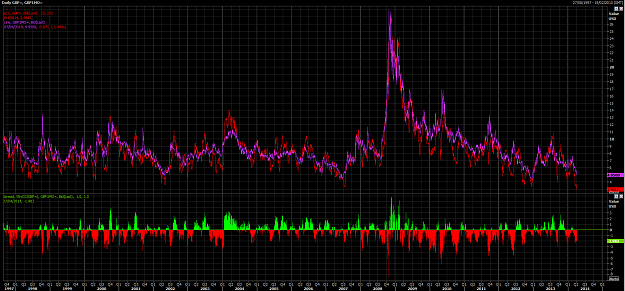

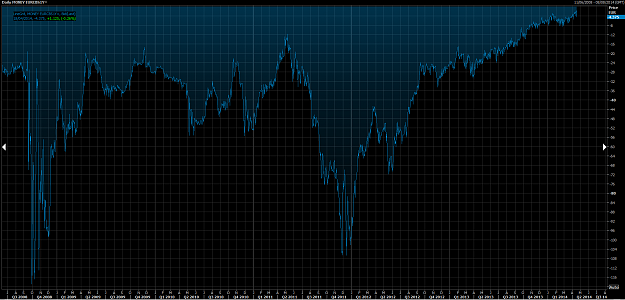

ATR doesn't really mean anything, but your point is valid, GBP vol is just so incredibly low Red line is prior 1 month volatility, it is 2.95 vol points which is lowest ever! Implied volatility for the next month is 4.95, not quite the lowest ever, ...

EURUSD