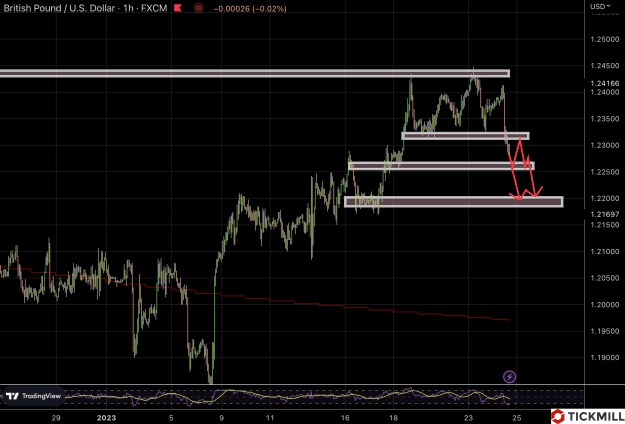

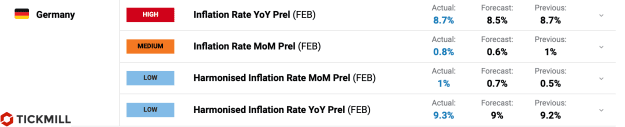

EURUSD presses against 1.08 level, market anticipates benign CPI print as energy inflation drops

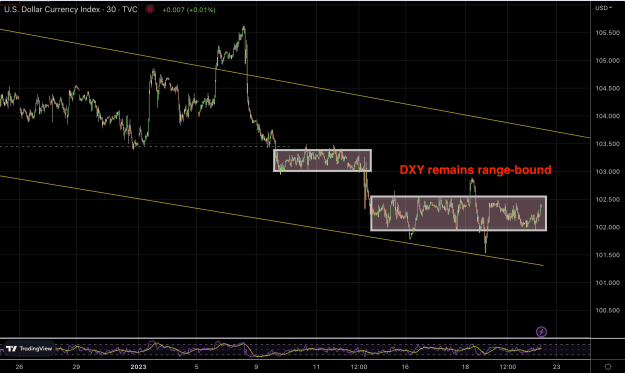

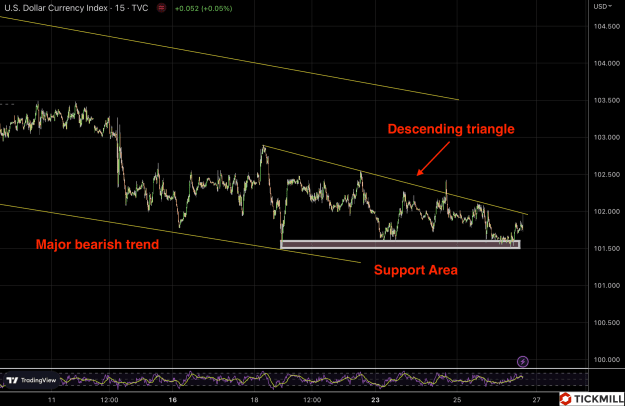

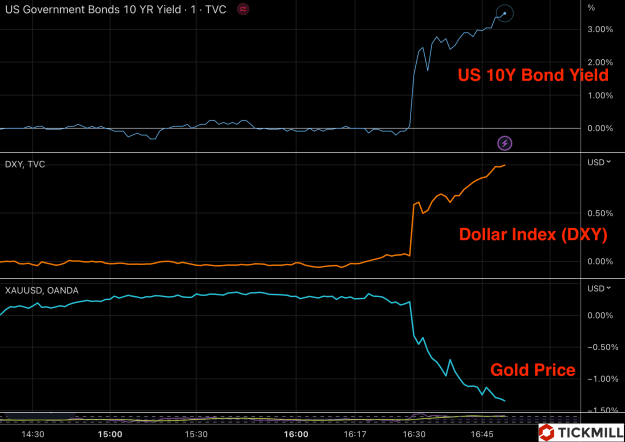

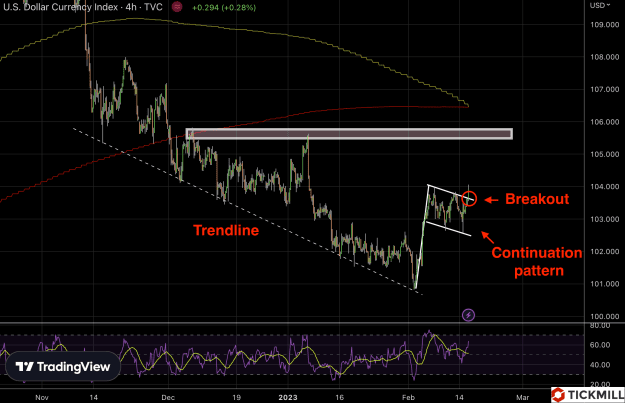

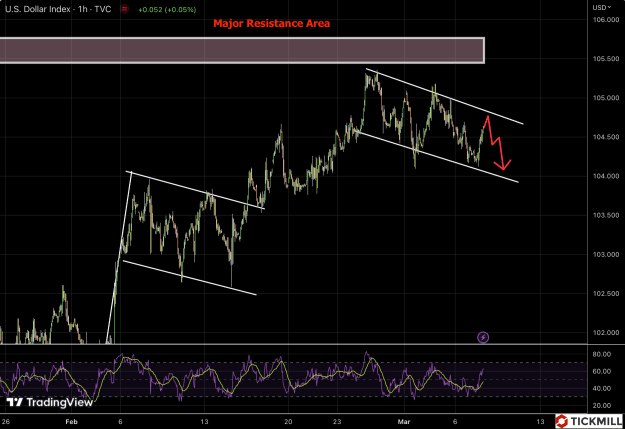

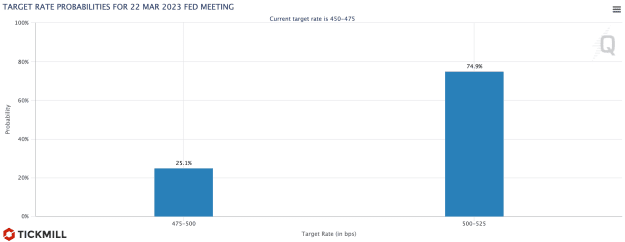

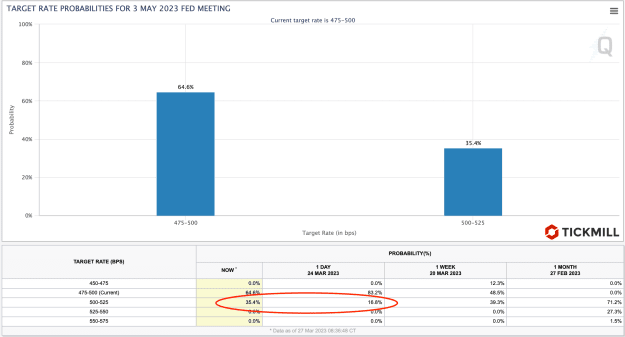

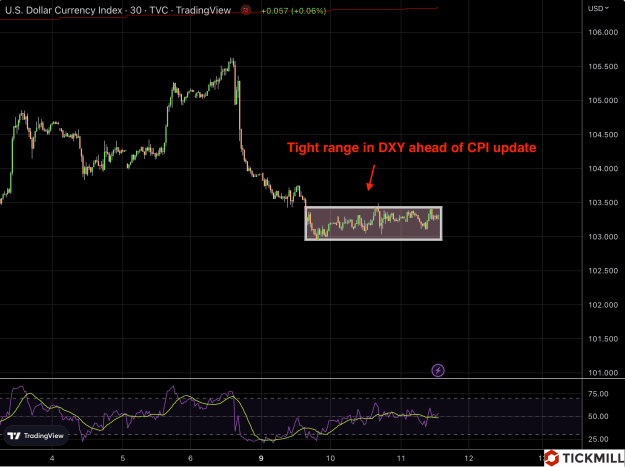

Risk appetite apparently grows in equity markets as Fed chief Powell did not take advantage of the Riksbank conference yesterday to repeat the recent mantra that a high inflation rate warrants further policy tightening. The market interpreted this as another signal that the Fed intends to slow down the pace of policy tightening, reaching “moderately restrictive level” in 1Q. The US market closed yesterday with moderate gains, futures continued to rally today, indicating potential bullish opening on the New York session today. Investors also increased demand for bonds, Treasury yields on the entire maturity spectrum trade slightly in the red today. The dollar index is clearly consolidating near the level of 103, buying interest remains low, there may be an attempt by sellers before the release of the CPI to press against the level of 103, and in case of bullish print, they may even break through the support and go towards 102.50 – 102 level:

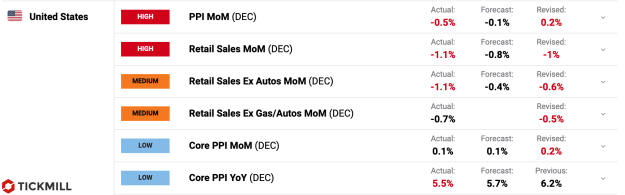

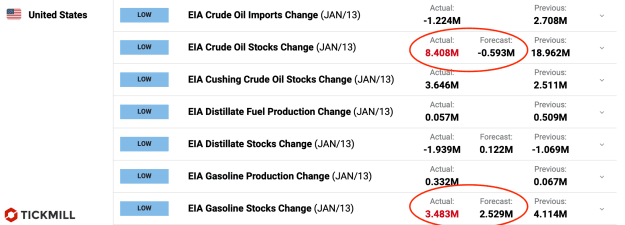

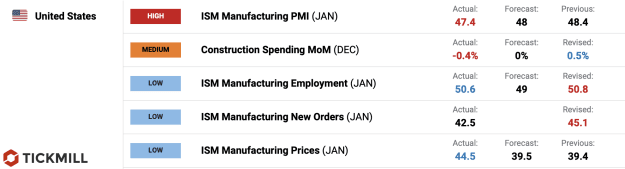

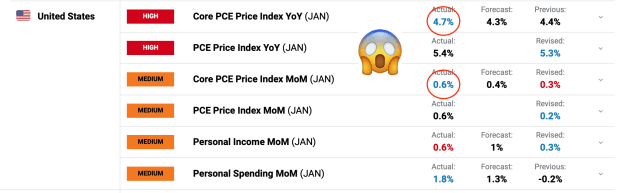

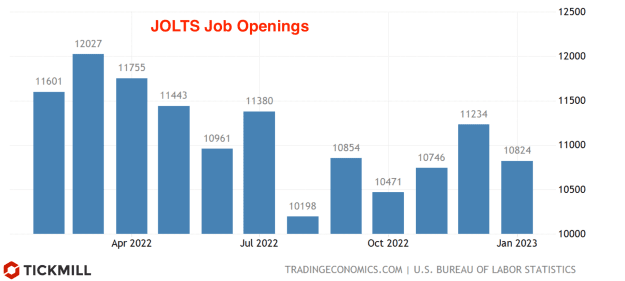

The market is clearly inclined now to price in decreasing hawkish vector of the Fed policy. The reason for this is an unexpectedly dovish print of ISM index for US non-manufacturing sector that we saw on Friday. The headline reading plunged to sub 50 area, which basically means contraction in activity compared to November. Industrial orders also declined - by 1.8%, which was a big surprise. The Small Index Optimism Index released yesterday by the NFIB fell from 91.9 to 89.8 points driven by small business expectations in business climate. Key highlights of the report include a decline in the share of firms planning to raise prices (a leading indicator of inflation) by 8%, and a decline in the share of firms expecting sales growth in real terms by 2%. However, the proportion of firms planning to hire staff remained high at 55%, among which 93% reported that there were few or no suitably qualified candidates in the market.

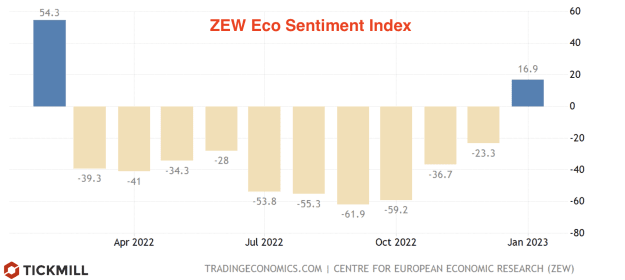

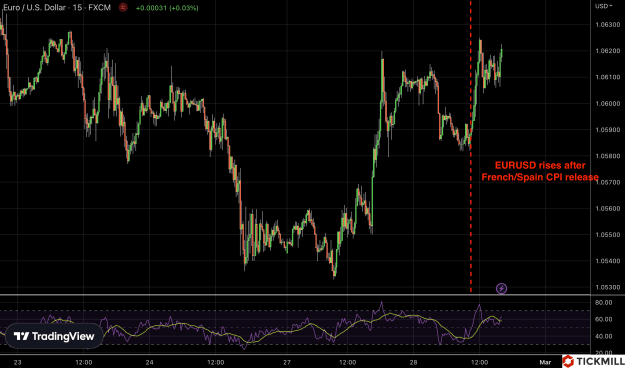

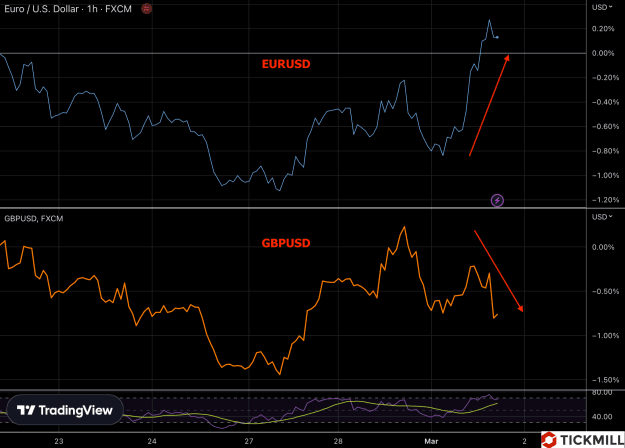

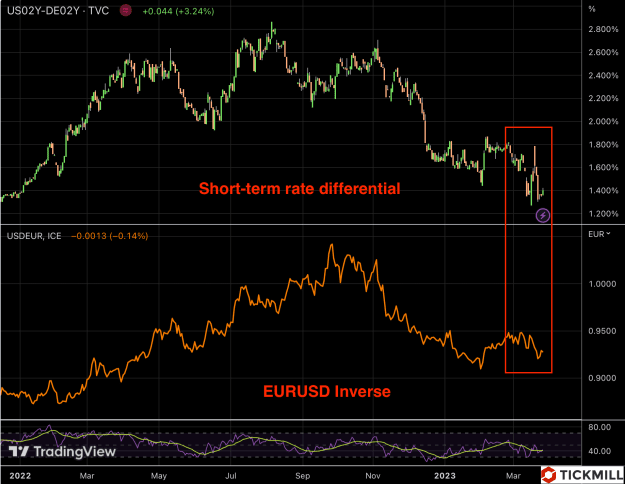

The mood for the European currency and European assets is gradually improving. Goldman abandoned the previous forecast of a recession in the EU in 2023, and European Commission official Gentilloni said that while the forecast for GDP growth in the first quarter of 0.3% remains relevant, the risks of lower or negative growth in Q4 2022 and Q1 2023 have noticeably decreased. ECB officials Schnabel and Centeno also changed their rhetoric, focusing on the fact that the peak of the inflationary shock in the energy market has passed, and the ECB is also getting closer to the end of rate hikes.

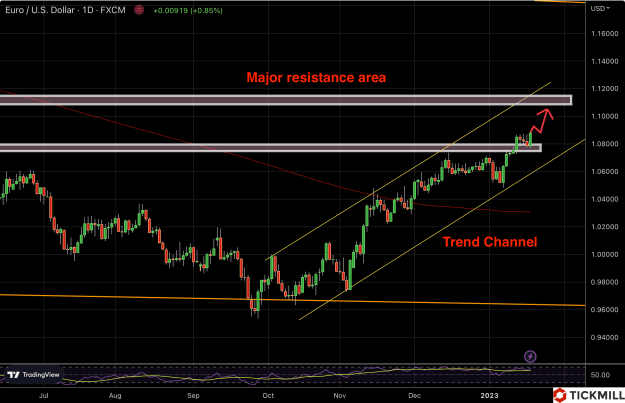

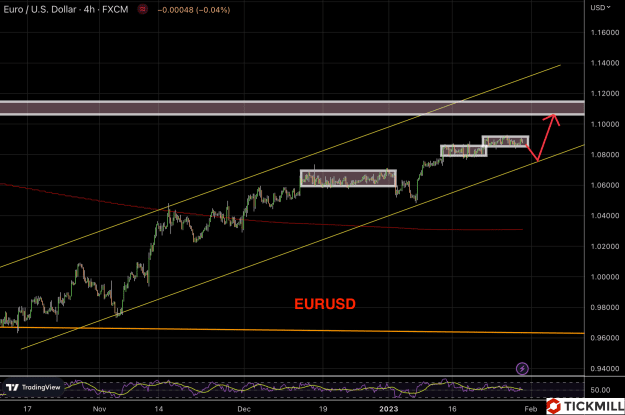

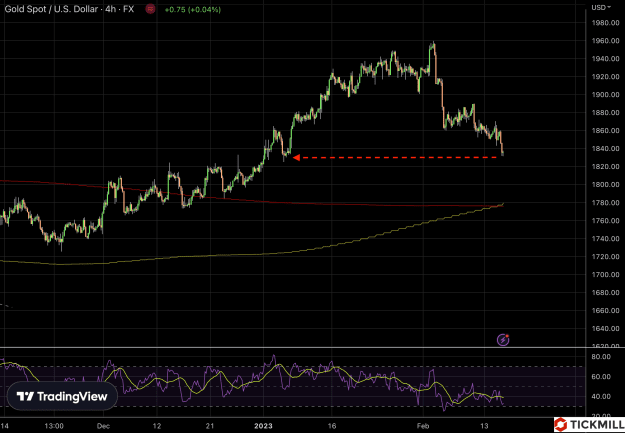

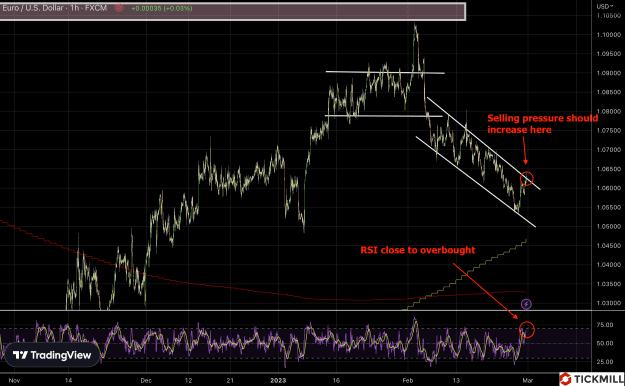

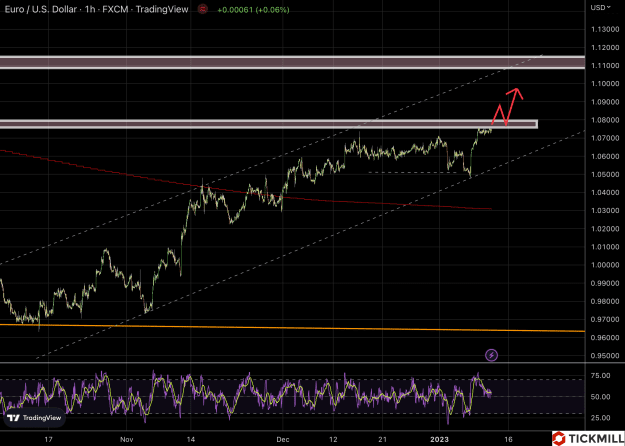

The technical setup for EURUSD is presented below:

The chart shows that the market keeps consolidating in a rather narrow range near the zone where major sell-off started in June 2022 (zone 1.08). This fact allows us to consider it as an area of short-term resistance. A favorable CPI print (5.7% or below in core inflation) will most likely allow the market to break through 1.08 level, after initial profit-taking on bullish breakout, the upward movement will most likely resume with a target of 1.09 and above. Buyers' interest is likely to drop noticeably near the 1.10 level, where the main bearish speculative momentum will likely emerge.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Risk appetite apparently grows in equity markets as Fed chief Powell did not take advantage of the Riksbank conference yesterday to repeat the recent mantra that a high inflation rate warrants further policy tightening. The market interpreted this as another signal that the Fed intends to slow down the pace of policy tightening, reaching “moderately restrictive level” in 1Q. The US market closed yesterday with moderate gains, futures continued to rally today, indicating potential bullish opening on the New York session today. Investors also increased demand for bonds, Treasury yields on the entire maturity spectrum trade slightly in the red today. The dollar index is clearly consolidating near the level of 103, buying interest remains low, there may be an attempt by sellers before the release of the CPI to press against the level of 103, and in case of bullish print, they may even break through the support and go towards 102.50 – 102 level:

Attached Image (click to enlarge)

The market is clearly inclined now to price in decreasing hawkish vector of the Fed policy. The reason for this is an unexpectedly dovish print of ISM index for US non-manufacturing sector that we saw on Friday. The headline reading plunged to sub 50 area, which basically means contraction in activity compared to November. Industrial orders also declined - by 1.8%, which was a big surprise. The Small Index Optimism Index released yesterday by the NFIB fell from 91.9 to 89.8 points driven by small business expectations in business climate. Key highlights of the report include a decline in the share of firms planning to raise prices (a leading indicator of inflation) by 8%, and a decline in the share of firms expecting sales growth in real terms by 2%. However, the proportion of firms planning to hire staff remained high at 55%, among which 93% reported that there were few or no suitably qualified candidates in the market.

The mood for the European currency and European assets is gradually improving. Goldman abandoned the previous forecast of a recession in the EU in 2023, and European Commission official Gentilloni said that while the forecast for GDP growth in the first quarter of 0.3% remains relevant, the risks of lower or negative growth in Q4 2022 and Q1 2023 have noticeably decreased. ECB officials Schnabel and Centeno also changed their rhetoric, focusing on the fact that the peak of the inflationary shock in the energy market has passed, and the ECB is also getting closer to the end of rate hikes.

The technical setup for EURUSD is presented below:

Attached Image (click to enlarge)

The chart shows that the market keeps consolidating in a rather narrow range near the zone where major sell-off started in June 2022 (zone 1.08). This fact allows us to consider it as an area of short-term resistance. A favorable CPI print (5.7% or below in core inflation) will most likely allow the market to break through 1.08 level, after initial profit-taking on bullish breakout, the upward movement will most likely resume with a target of 1.09 and above. Buyers' interest is likely to drop noticeably near the 1.10 level, where the main bearish speculative momentum will likely emerge.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.