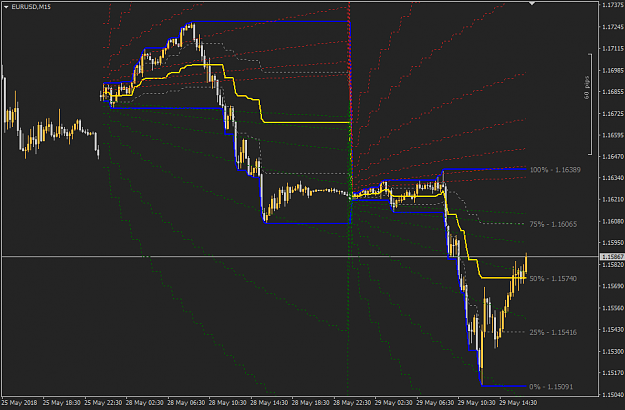

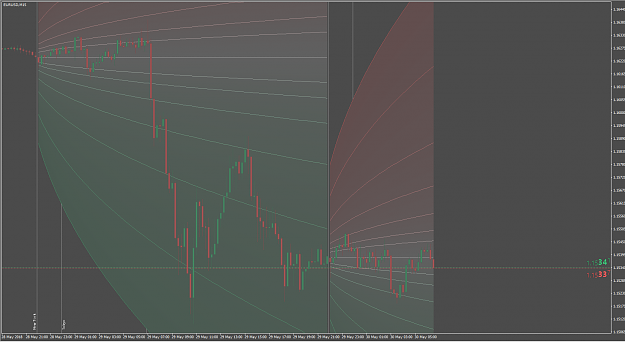

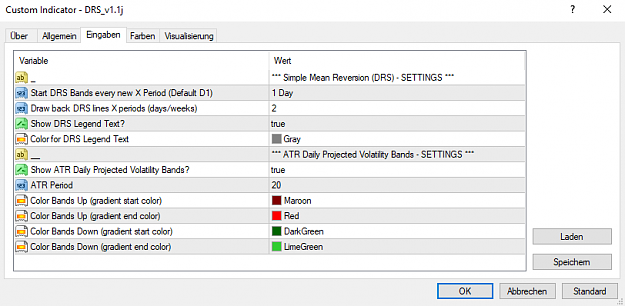

Here is my first variant of the DRS indicator which also has the possibility to show the mentioned atr based projected volatility bands {image} {image} {file}

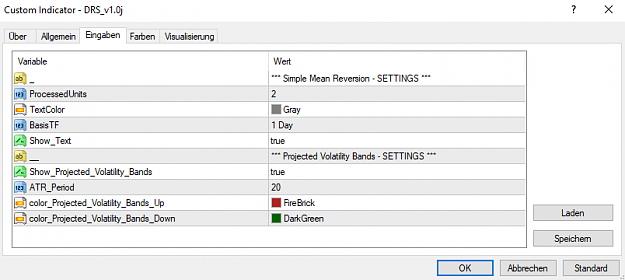

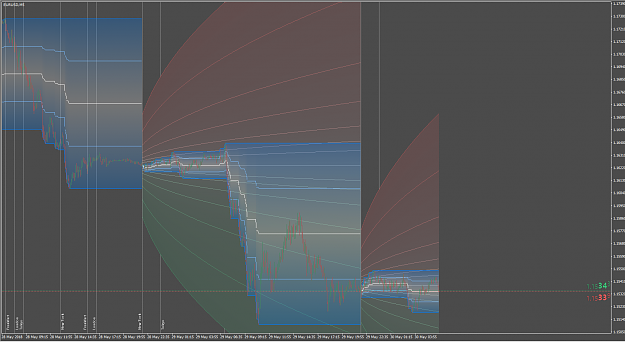

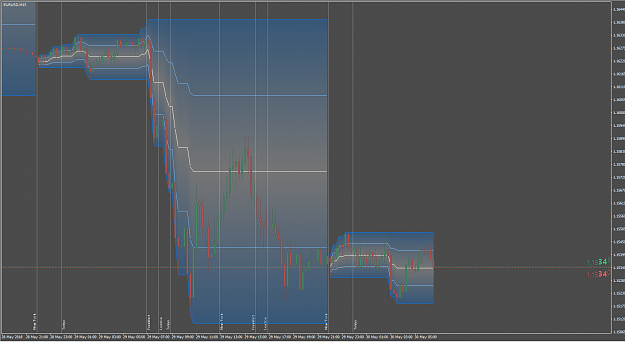

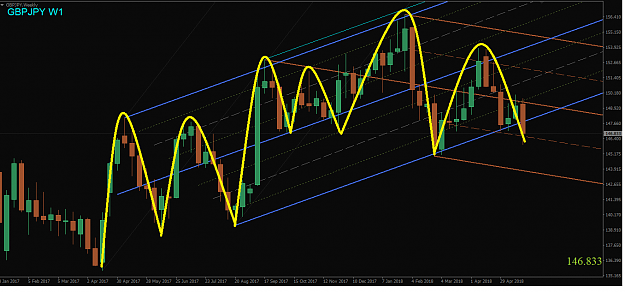

My friend Jagg showed me this thread and i could not resist. If it's useful i will stay and try to improve it with your all help. You have to option to toggle all at will. Change colors and opacity to fit your needs. {image} {image} {image} 2828209 I will follow this now, so feel free to request improvements. Updated version with better performance while painting all the stuff (sorry for that). {file}

Ignored

Nice.

What type of drawing method you use? Initially I wanted to use DRAW_FILLING but unfortunately for some reason I cant make it work in MQL4. (It only works with mql5).

{quote} Nice. {quote} Nice. What type of drawing method you use? Initially I wanted to use DRAW_FILLING but unfortunately for some reason I cant make it work in MQL4. (It only works with mql5).

Ignored

Thx.

I builded up my own graphical library for MT4, so i'm indepent from the MT4 developer team (it's total rubbish to add features in the language but not to implement them fully).

I have a few questions that I was hoping OP could help answer:

1) Are there other ways to determine the start/end of a cycle apart from the hours? (Or would 00hrs-23hrs the "universal cycle"?)

2) Are some cycles longer/shorter in certain pairs compared to others? How would you determine this? Sessions, maybe? Overlapping sessions maybe?

3) What are your typical drawdown percentages like?

I would like to ask about the time GMT+2.

I downloaded history data from tickstory without shift of time and put it into MT4 without shift. What i got is that at most of the year the trading week starts at 21:00 and ends at 21:00 and a little part of the year starts and ends at 22:00. and the days monday and friday are partial days- less than 24 hours. When i put the prices in MT4 with shift of 2 hours there is something strange. For H1, at summer the week stats and end at 23:00, and at winter 00:00. But for the daily the day always starts at 02:00.

What should i do?

Another question about the GMT+2:

I put in the data as i described at former post. And added indicator TM_DRS (by jensitzig). Since the daily starts at 02:00, the day of the indicator also starts at 02:00, which is not the start of the trading day.

May someone help?

Thanks,

Avraham

Hi! I would like to ask about the time GMT+2. I downloaded history data from tickstory without shift of time and put it into MT4 without shift. What i got is that at most of the year the trading week starts at 21:00 and ends at 21:00 and a little part of the year starts and ends at 22:00. and the days monday and friday are partial days- less than 24 hours. When i put the prices in MT4 with shift of 2 hours there is something strange. For H1, at summer the week stats and end at 23:00, and at winter 00:00. But for the daily the day always starts at...

Ignored

There are only 2 kinds of shift. First brokers with GMT time without shift (very easy because it's the standard). But kkep in mind UTC will be shifted 1 hour when daylight saving is on in europe. The other brokers have GMT+2 to achieve that the "trading week" starts monay 0:00 and end friday 23:59.

Then we have the 2 weeks when american daylight saving is already on or still on and europe hasn't daylight saving. Then all brokers shifting 1 hour that the american session of friday ends 23:59 this comes with the problem that the week starting on sunday even for GMT+2 brokers.

That's why i normalize all my time information in the programs and always calculating the higher TFs from the H1 data. That's the only way to have the same calculation between GMT or GMT+2 brokers. The shift will be also calculated for every week, fortunately there are fix rules for the daylight saving in europe and america.

Hi!

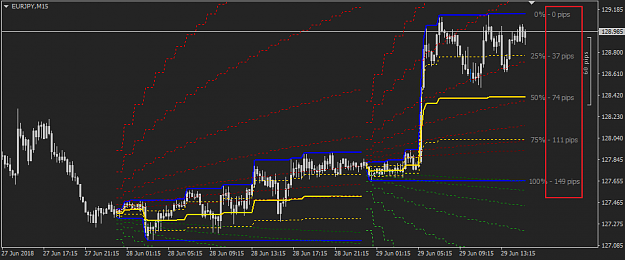

After my 2 last posts: it is very interesting. In both cases: when i put in the prices without shift and day started at 21:00, and when the day starts at 02:00:

well, in both cases i see the same: when price arrives at level 4 ( and even when it arrives at level 3 in a very early hour of the day), it usually reverses towards the open price.

However. it is just first observation, not backtesting.

{quote} Some people will argue that this is a classic case of Gambler's fallacy However, I'm not completely convinced about the validity of this theory in the context of trading.

Ignored

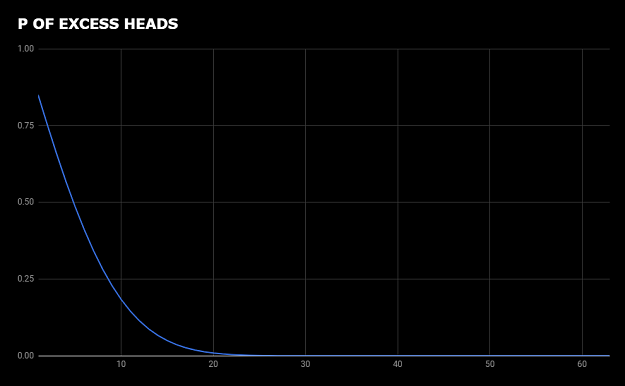

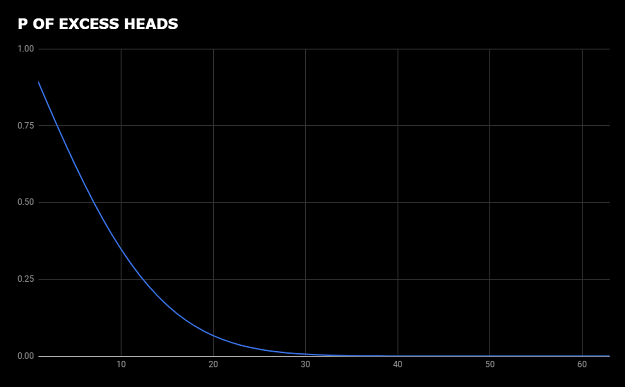

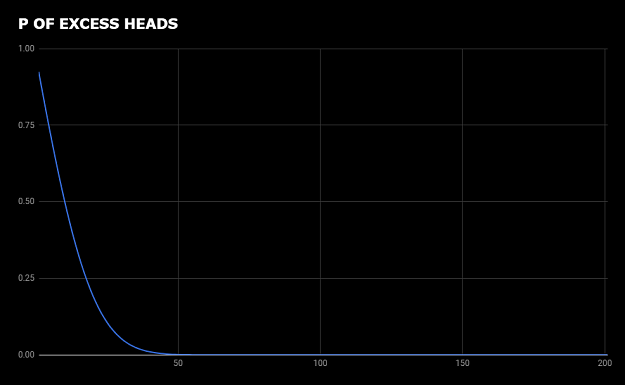

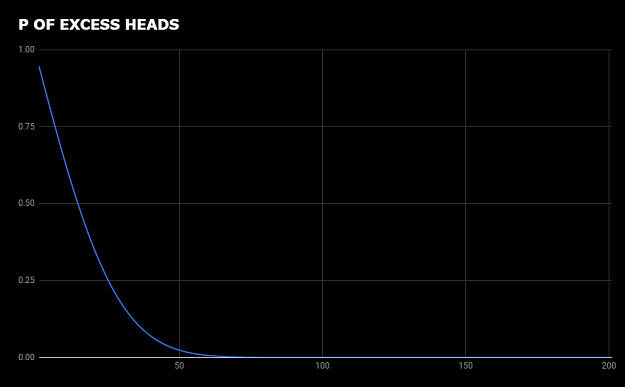

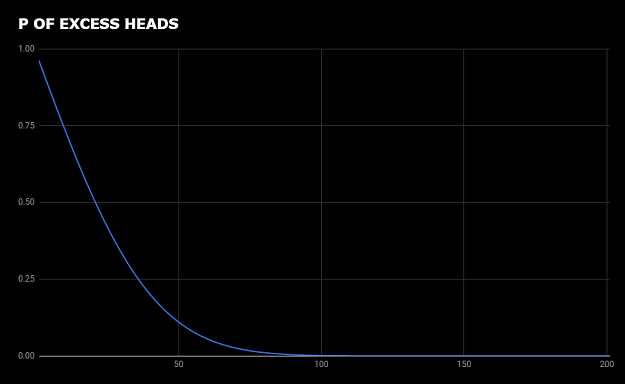

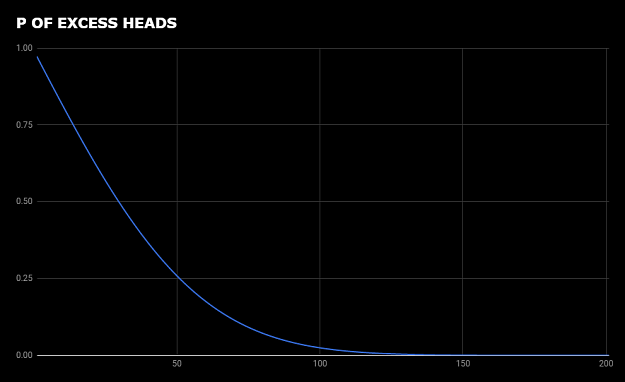

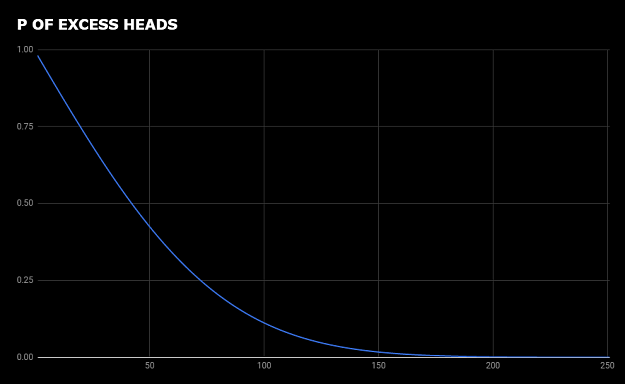

I am fascinated with the probabilities, and I also have doubts about certain aspects of the Gambler's fallacy and trading.

For fun, here are the probabilities of getting an excess of x heads in a sample of y flips. Nothing special, but just interesting to see how the distribution widens.

{quote} There are only 2 kinds of shift. First brokers with GMT time without shift (very easy because it's the standard). But kkep in mind UTC will be shifted 1 hour when daylight saving is on in europe. The other brokers have GMT+2 to achieve that the "trading week" starts monay 0:00 and end friday 23:59. Then we have the 2 weeks when american daylight saving is already on or still on and europe hasn't daylight saving. Then all brokers shifting 1 hour that the american session of friday ends 23:59 this comes with the problem that the week starting...

Ignored

Thanks for your reply.

I don't know to read and write code.

However, if you calculate from H1, i don't understand why do i get the start of day at 02:00 in your indicator? But i simply deleted the daily data, that shows day start at 02:00, and then your indicator works well. Day start at 0:00.

Thanks!

{quote} Thanks for your reply. I don't know to read and write code. However, if you calculate from H1, i don't understand why do i get the start of day at 02:00 in your indicator? But i simply deleted the daily data, that shows day start at 02:00, and then your indicator works well. Day start at 0:00. Thanks!

Ignored

That‘s very easy. Since the rules are not mine I used the exact ones from this thread. So I don‘t have activated the calculation for that shift to be compatible to the other tools (like from jagg)

@jensitzig:

That's why i normalize all my time information in the programs and always calculating the higher TFs from the H1 data. That's the only way to have the same calculation between GMT or GMT+2 brokers. The shift will be also calculated for every week, fortunately there are fix rules for the daylight saving in europe and america

Hi!

What are the rules to calculate every week?

Thanks,

Avraham